Why traditional KYC breaks down

The standard model for identity verification relies on a fragile premise: that a central server can securely store highly sensitive personal data indefinitely. This approach creates single points of failure that are increasingly difficult to defend against sophisticated cyber threats. When a KYC provider stores passports, bank statements, or proof of residence, they become prime targets for data breaches. The exposure of this data does not just harm users; it exposes platforms to severe regulatory liability and reputational damage.

This centralization is the core weakness that ZK KYC Systems guide addresses. Traditional systems require the verifier to see the data to validate it. Zero-knowledge proofs change this dynamic by allowing a user to prove they meet specific criteria—such as being over 18 or residing in a permitted jurisdiction—without revealing the underlying personal data. This shift eliminates the need for a central repository of sensitive documents, thereby removing the primary incentive for attackers.

As the digital economy matures, the cost of maintaining secure, centralized identity infrastructures continues to rise. The liability associated with holding user data often outweighs the benefits of the verification process itself. By moving toward privacy-first compliance, platforms can reduce their attack surface while still meeting regulatory requirements. This is not just a technical upgrade; it is a fundamental restructuring of how trust is established in digital interactions.

How ZK KYC Systems Actually Work

Traditional KYC asks you to hand over your passport, selfie, and proof of address to a central database. Zero-Knowledge Proof KYC (ZK-KYC) flips this model. Instead of storing your raw data, the system allows you to prove you meet specific compliance criteria—like being over 18 or residing in a permitted jurisdiction—without revealing the underlying personal information. As Treza Labs defines it, this infrastructure enables applications to verify that a user meets compliance requirements without exposing or storing personal data. This shift moves the burden of privacy from the service provider to the cryptographic protocol itself.

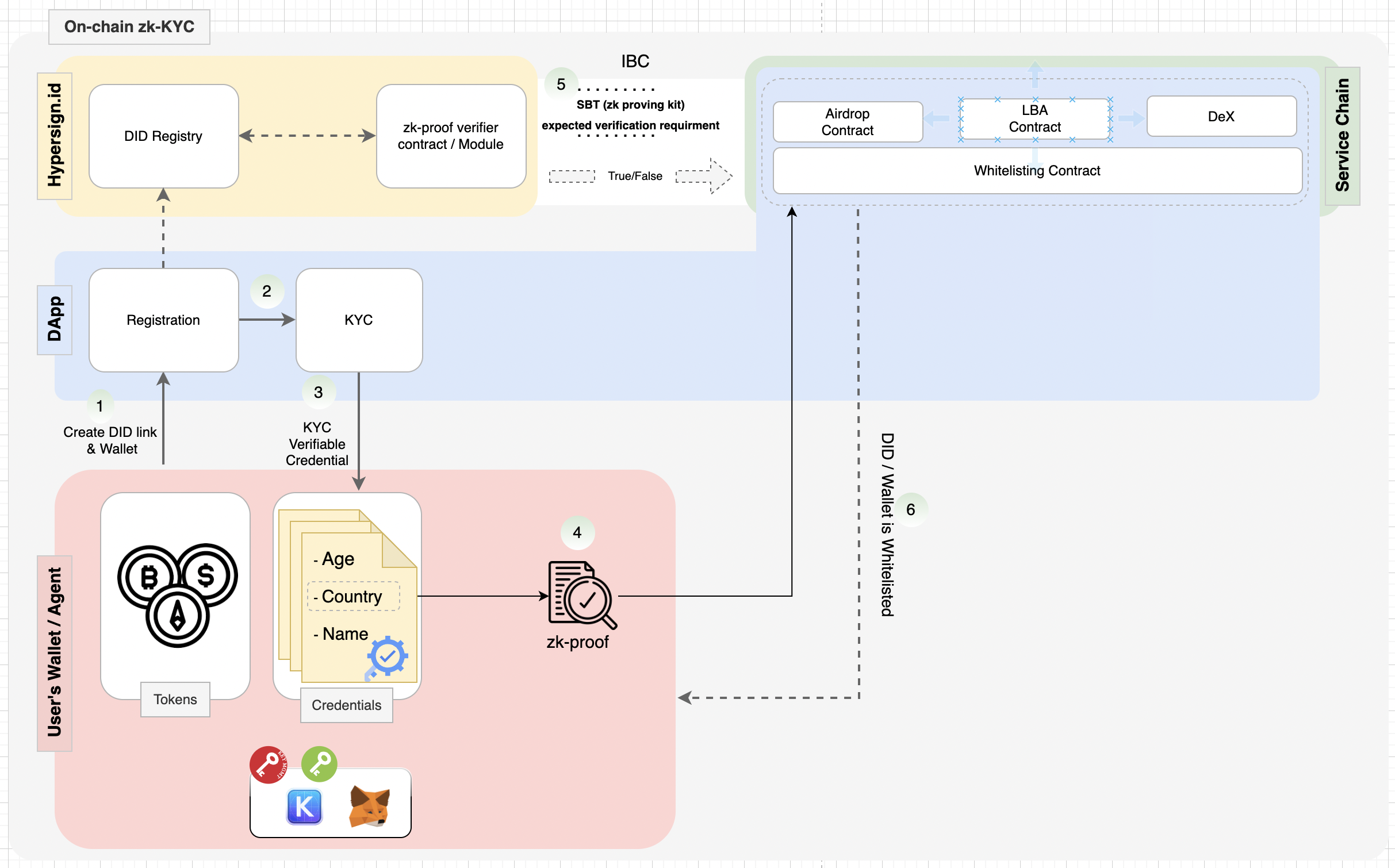

The process begins with a trusted setup, often involving a decentralized network of entities that generate cryptographic parameters. Once established, these parameters create a "ZK-KYC registry." When you undergo identity verification through a trusted issuer (like a government agency or a licensed bank), that issuer signs a credential attesting to your attributes. You then use a specialized application to generate a zero-knowledge proof. This proof is a unique cryptographic artifact that demonstrates the validity of your signed credential against the public registry parameters, without disclosing the credential's content.

Think of this proof as a sealed envelope that the verifier can check without opening. The verifier can confirm the envelope contains a valid, signed credential from an authorized issuer and that it satisfies specific conditions (e.g., "age > 18"), but they cannot see your name, birthdate, or address. This mechanism ensures that the "Service Chain" or DeFi application only receives the binary result: compliant or not. It effectively decouples identity verification from identity exposure, allowing for privacy-preserving compliance.

The final step is on-chain verification. The generated proof is submitted to a smart contract, which checks its mathematical validity against the public parameters. If the proof is valid, the contract emits an event or updates a state variable indicating the user is verified. This creates a reusable, privacy-first compliance status that can be checked by multiple applications without re-submitting personal data. As noted by Chainlink, designing these systems to offer privacy by default while accommodating regulatory requirements avoids the creation of vulnerable "master keys" that could compromise user data.

Comparing leading ZK KYC vendors

Choosing the right ZK KYC Systems guide implementation requires looking past marketing claims to understand how each vendor handles data retention, verification speed, and regulatory alignment. While the goal is the same—verifying compliance without exposing raw personal data—the architectural trade-offs differ significantly between Treza, Zyphe, and zkPass.

Treza: Infrastructure for Regulated Finance

Treza positions itself as a backend infrastructure layer specifically designed for crypto and regulated finance applications. Their approach focuses on providing a ZK-KYC framework that allows applications to verify that a user meets compliance requirements without storing or exposing personal data. This makes them a strong candidate for platforms that need to integrate privacy-preserving verification into their existing compliance workflows without building custom zero-knowledge circuits from scratch.

Zyphe: Production-Grade Speed and No Retention

Zyphe emphasizes the operational reality of deploying zero-knowledge proofs in production KYC environments. Their architecture is built for regulator-grade verification with sub-second performance, addressing the latency issues that often plague ZK implementations. Crucially, Zyphe operates with a no-document-retention policy, meaning the heavy lifting of verification happens in a way that leaves no persistent record of the user’s sensitive documents, reducing liability and storage overhead for the integrating platform.

zkPass: Decentralized Identity and Compliance

zkPass takes a different angle by focusing on decentralized identity and compliance use cases. Their documentation highlights the risks of traditional KYC service providers that require the storage of passports, bank statements, or proof of residence, creating high-value targets for data breaches. By shifting the verification model to one where data exposure is minimized through decentralized methods, zkPass appeals to projects prioritizing user sovereignty and data minimization as a core compliance feature.

| Vendor | Primary Focus | Data Retention | Verification Speed |

|---|---|---|---|

| Treza | Infrastructure for Crypto/Finance | Minimal/None | Standard |

| Zyphe | Production KYC Verification | No Document Retention | Sub-second |

| zkPass | Decentralized Identity | Decentralized/Minimal | Variable |

Regulatory readiness in 2026

The legal landscape for ZK KYC Systems is shifting from theoretical compliance to operational necessity. By 2026, major regulatory frameworks like the EU’s eIDAS 2.0 and the U.S. Anti-Money Laundering Act (AMLA) are no longer distant proposals but active requirements that demand precise, auditable identity verification without exposing sensitive personal data.

The core challenge for institutions is the "lawful intercept" model. Regulators need to verify compliance—such as confirming a user is over 18 or not on a sanctions list—without receiving the underlying personal information. ZK KYC Systems solve this by allowing a verifier to check a cryptographic proof. If the proof holds, the system confirms compliance; if not, it rejects it. The regulator sees only the pass/fail result, not the user’s passport or address.

This approach aligns with eIDAS 2.0’s push for decentralized identity wallets. Instead of storing data in centralized silos that are prone to breaches, users hold their credentials in a digital wallet. When a service requires KYC, the user presents a zero-knowledge proof. This satisfies the legal requirement for "knowing" the customer while adhering to privacy principles that minimize data collection.

For financial institutions, this means moving away from bulk data storage. Compliance becomes a matter of verifying cryptographic signatures against regulatory standards. It reduces liability, minimizes the attack surface for data breaches, and positions ZK KYC as the standard for privacy-first compliance in 2026.

Implementing ZK KYC in your stack

Integrating ZK KYC Systems into your infrastructure requires shifting from traditional data storage to cryptographic verification. The goal is to let users prove compliance—such as being over 18 or located in a permitted jurisdiction—without exposing their underlying identity documents on-chain.

Start by selecting a zero-knowledge circuit framework like Circom or Halo2. These tools allow you to define the logic for your proofs. You will need to encode your compliance rules into a circuit that accepts private inputs (the user's data) and outputs a public boolean result.

Write the circuit logic that validates the user's attributes. For example, a circuit might check if a hash of a government ID matches a trusted issuer's signature and if the birth date satisfies an age threshold. This circuit becomes the core of your ZK KYC Systems guide implementation.

Users generate proofs on their devices using their private data. This ensures that sensitive personal information never leaves their device. The proof is a short cryptographic string that mathematically guarantees the circuit was executed correctly on valid inputs.

Submit the proof to a smart contract or an off-chain verifier. The verifier checks the proof against the public parameters of the circuit. If valid, the system grants access or mints a Soulbound Token (SBT) representing the verified status, completing the ZK KYC workflow.

This approach minimizes data liability and aligns with privacy-first regulatory trends. By focusing on the proof rather than the data, you build a more secure and user-centric compliance layer.

Frequently asked questions about ZK KYC

Zero-Knowledge Proof KYC (ZK-KYC) is a privacy-preserving verification method where a user proves they meet specific regulatory criteria—such as age or jurisdiction—to a verifier without revealing underlying personal data. Instead of uploading sensitive documents to a central server, a licensed identity provider verifies your credentials once and issues a cryptographic proof. This allows platforms to comply with regulations while ensuring no master key or raw data is stored, effectively separating identity from transaction history.

The standard KYC process typically follows five distinct stages: Customer Identification Program (CIP), Customer Due Diligence (CDD), Risk Assessment, Ongoing Monitoring, and Reporting Suspicious Activities. ZK-KYC systems integrate into this workflow by automating the verification and risk assessment phases. By using zero-knowledge proofs, these systems can confirm that a user passes CDD checks without storing the underlying documents, reducing the attack surface for data breaches while maintaining audit trails for regulators.

Buying cryptocurrency without KYC is legal in most jurisdictions, though tax obligations still apply regardless of the purchase method. However, as ZK-KYC systems mature, the gap between anonymous trading and compliant participation narrows. Users can now access regulated financial products with the same privacy guarantees they expect from decentralized protocols, making non-KYC trading less necessary for those prioritizing data protection.

No comments yet. Be the first to share your thoughts!