Why traditional KYC breaks down

The current standard for Know Your Customer (KYC) verification relies on centralized databases that store sensitive personal documents like passports, proof of residence, and bank statements. This model creates a single point of failure: a massive, high-value target for attackers. When a centralized provider is breached, the exposed data includes not just names, but biometric and financial records that cannot be changed, leaving users with permanent identity risk.

Beyond security, this architecture fragments data into silos. Users must repeat the verification process for every new platform, uploading the same documents repeatedly. This friction increases abandonment rates and creates a poor user experience, as compliance becomes a barrier rather than a seamless background process. The system prioritizes data hoarding over actual risk mitigation.

Zero-Knowledge KYC Systems guide the industry away from this vulnerable model. Instead of storing raw data, these systems use cryptographic proofs to verify that a user meets specific regulatory criteria—such as age or jurisdiction—without ever revealing the underlying personal information. This shift eliminates the central database, removing the incentive for attackers and restoring privacy to the verification process.

How ZK KYC actually works

Zero-Knowledge Proof KYC (ZK-KYC) shifts the verification paradigm from data collection to cryptographic proof. Instead of uploading passports or utility bills to a centralized database, users prove they meet specific regulatory predicates—such as being over 18 or residing in a permitted jurisdiction—without revealing the underlying personal identifiable information (PII).

This process relies on a "Lawful Intercept" model where a trusted identity provider (IdP) acts as the initial verifier. Once the IdP confirms your identity through traditional means, they issue a signed credential. You then use this credential to generate a zero-knowledge proof, demonstrating compliance to a service provider while keeping your actual identity data private.

The mechanism ensures that sensitive documents are never stored on-chain or by the application requesting the check. This eliminates the risk of massive data breaches while satisfying regulatory requirements for age and location verification.

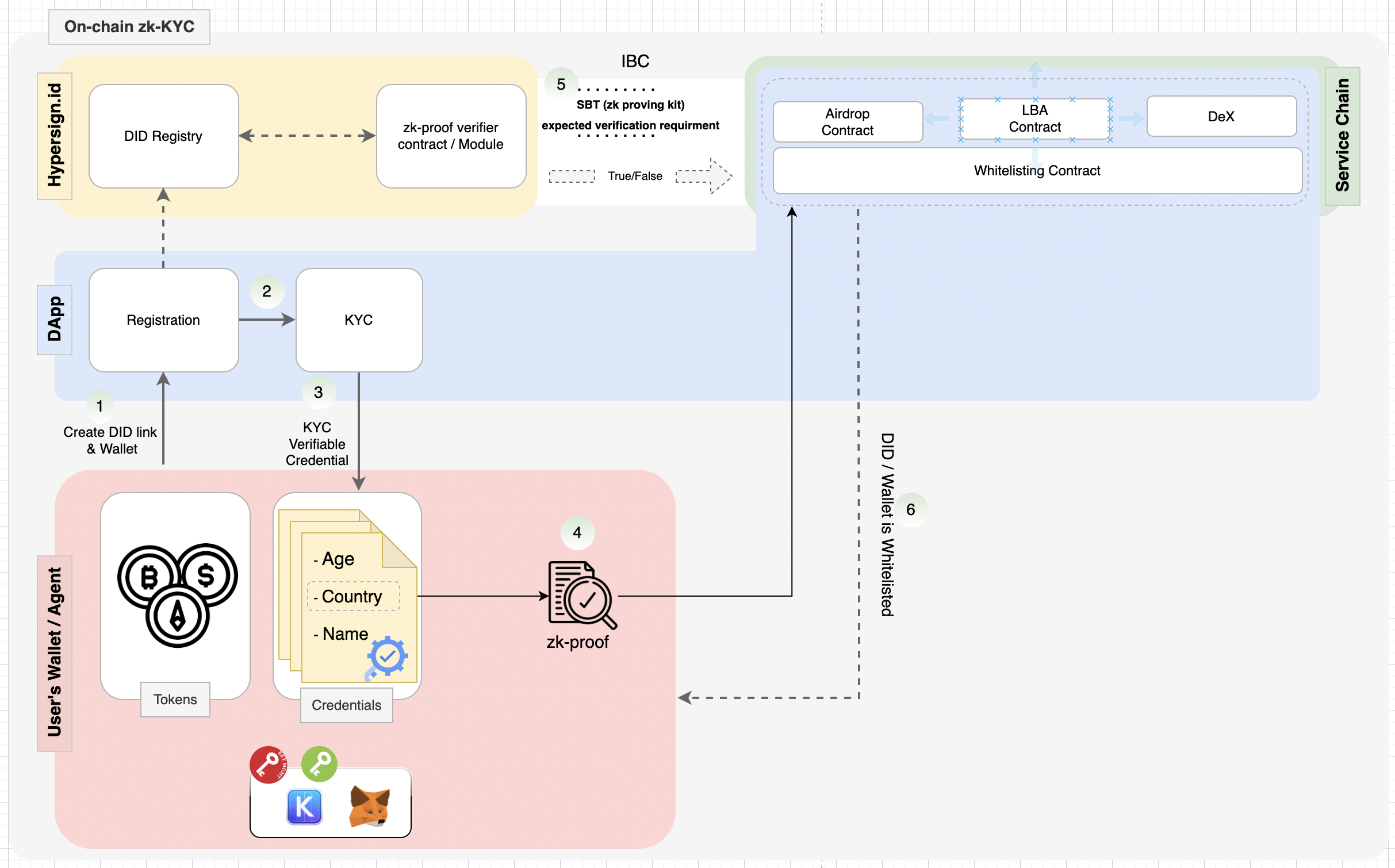

The Verification Flow

The technical architecture follows a strict sequence to ensure both privacy and compliance. Here is how the proof generation and verification steps unfold in a typical ZK KYC system.

The process begins with a licensed identity provider, such as a government agency or certified KYC vendor. They verify your documents through standard channels. Once verified, they issue a signed digital credential attesting to your identity attributes, such as age or residency status.

The service provider defines the specific conditions required for access. These are called predicates. Common examples include "Age > 18" or "Country Code = US." The system translates these legal requirements into mathematical constraints that the zero-knowledge proof must satisfy.

Using your signed credential, your device generates a zero-knowledge proof. This cryptographic artifact proves that the data in your credential satisfies the provider's predicates without exposing the actual data. The proof is created locally, ensuring your raw identity details never leave your device.

The generated proof is submitted to a smart contract or verifier service. The contract checks the cryptographic validity of the proof against the provider's public key and the defined predicates. If the proof is valid, the contract issues a non-transferable token or status indicating you are verified.

As an Amazon Associate, we may earn from qualifying purchases.

This separation of concerns allows financial applications to comply with anti-money laundering (AML) and know-your-customer (KYC) regulations without becoming targets for data theft. The user retains control over their digital identity, sharing only what is legally necessary for each specific interaction.

Core Infrastructure Components

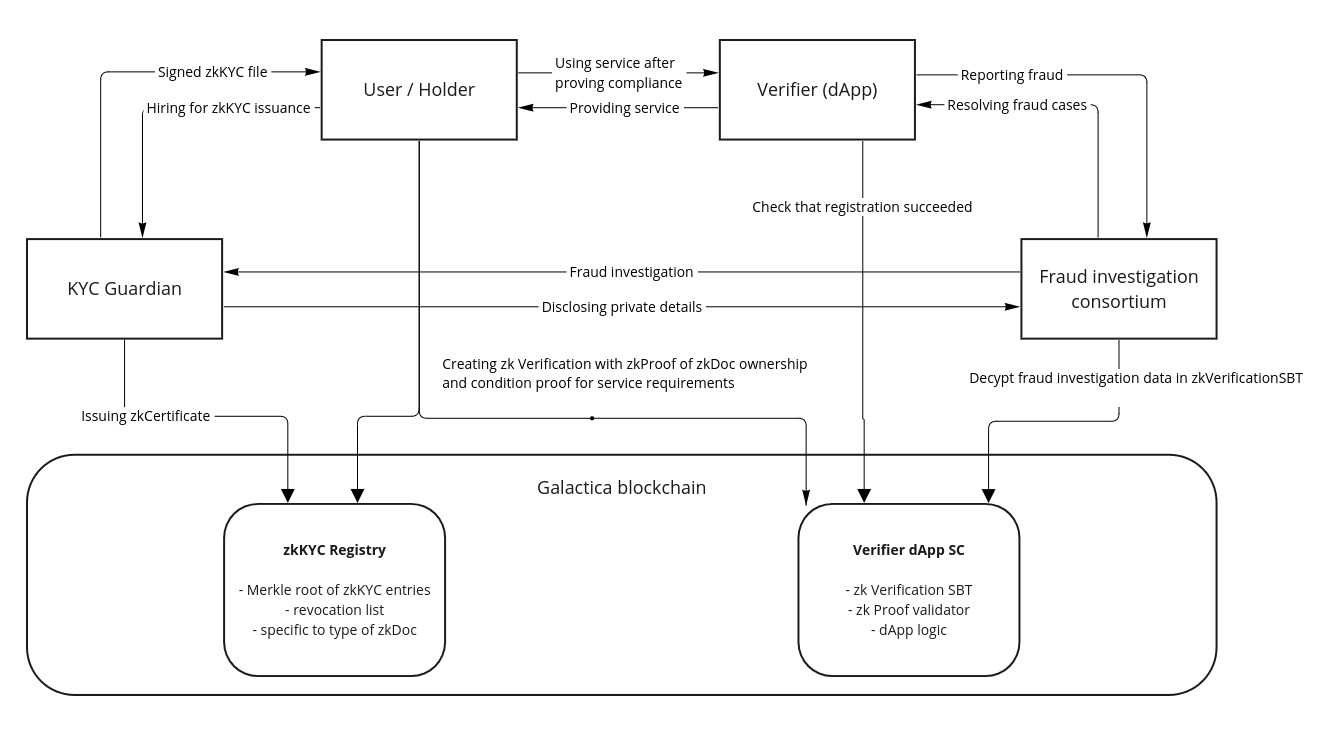

Building a ZK KYC Systems guide requires mapping out a stack that separates identity generation from verification. Unlike traditional databases that store PII, this architecture relies on cryptographic proofs to validate compliance status. The system rests on three pillars: Identity Providers (IPs) that perform the initial check, ZK Circuit builders that generate the proof, and Verifiers that enforce the rules on-chain.

Identity Providers (IPs)

The Identity Provider is the trusted anchor of the stack. It performs the actual Know Your Customer check—verifying passports, biometrics, or sanctions lists—against regulatory standards. The IP issues a signed credential attesting that the user passed the check, but it does not generate the zero-knowledge proof itself. This separation ensures that the verifier never sees the raw identity data.

Popular IPs include regulated entities like Jumio or Onfido, as well as decentralized identity issuers. The critical metric here is not just verification speed, but the trust model: does the IP hold your data, or does it issue a revocable credential? For ZK KYC, the IP acts as the "source of truth" that the circuit will eventually reference.

ZK Circuit Builders

Circuit builders are the engines that translate identity claims into zero-knowledge proofs. A circuit is a set of mathematical constraints that define what is provable. For example, a circuit might prove that "the credential was signed by IP X" AND "the birth date is before 2005" without revealing the actual birth date or the IP's signature.

Developers use frameworks like Circom, Gnark, or Halo2 to write these circuits. The complexity lies in optimizing the circuit for gas efficiency on-chain. If the circuit is too heavy, the proof generation becomes slow and expensive. The goal is to create a "predicate"—a specific condition (like age or residency) that can be verified instantly by a smart contract.

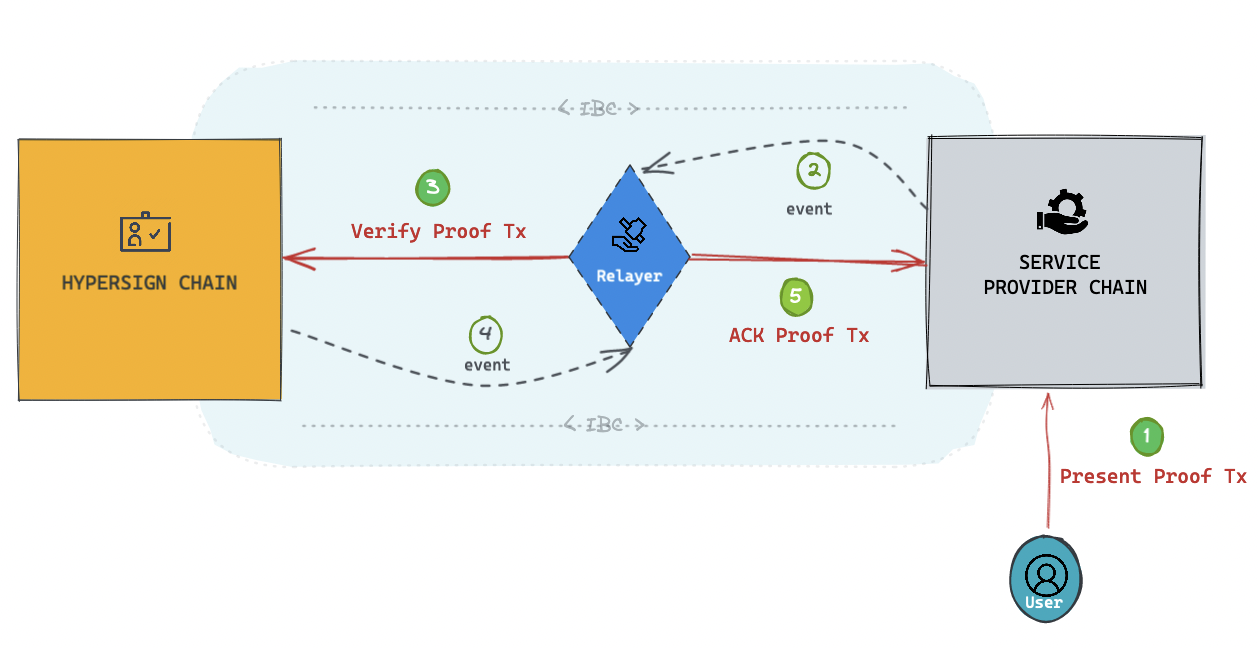

Verifiers and Smart Contracts

The verifier is the final gatekeeper, typically deployed as a smart contract on a blockchain. It receives the ZK proof and the public inputs (the predicate values) from the user. The contract runs a verification algorithm to ensure the proof is mathematically valid.

If the proof holds, the contract emits an event or mints a Soulbound Token (SBT) representing the verified status. This allows dApps to query the contract to check if a user is compliant without ever contacting the user directly. The verifier must also handle revocation: if the Identity Provider revokes a credential, the contract must reject proofs associated with that ID.

Infrastructure Comparison

Selecting the right stack depends on your latency requirements and trust assumptions. The table below compares common infrastructure patterns.

Strategic implementation steps

Integrating ZK KYC into a dApp requires a shift from traditional data storage to cryptographic verification. Instead of collecting and storing PII, your protocol acts as a verifier of zero-knowledge proofs. This workflow ensures compliance with regulations like GDPR and AML laws without becoming a single point of failure for user data.

Before writing code, specify exactly what the user must prove. Common criteria include age over 18, residency in a permitted jurisdiction, or blacklist status. The circuit logic must be precise; if the proof requirements are too broad, you risk rejecting legitimate users, while too narrow a scope may fail regulatory audits.

Choose a proving system like Circom, SnarkJS, or Halo2. Your stack must support the specific arithmetic or boolean operations required by your circuit. Ensure the verifier contract (for on-chain validation) or off-chain verifier is compatible with your protocol’s existing infrastructure. This choice dictates the gas costs and proof generation time.

Connect your frontend to a trusted identity issuer (e.g., Civic, Polygon ID, or a centralized KYC provider). The user submits their documents to the issuer. Once verified, the issuer signs a credential. Your dApp then uses this credential to generate the ZK proof locally on the user’s device, ensuring the issuer never sees the final proof submitted to your protocol.

For on-chain protocols, deploy a smart contract that contains the verification logic. This contract must accept the ZK proof and the public inputs (e.g., the user’s address and the specific claim being verified). Implement strict access controls to prevent replay attacks and ensure that only valid proofs grant access to protocol features like staking or airdrops.

Zero-knowledge circuits are complex and prone to subtle bugs. Conduct rigorous unit testing on the circuit logic and perform a formal security audit. Verify that the proof generation does not leak any side-channel information. This step is critical for maintaining user trust and ensuring that your ZK KYC system remains robust against adversarial inputs.

Common pitfalls and fixes

Implementing a ZK KYC Systems guide often reveals gaps between theoretical privacy and operational reality. The most frequent friction points involve circuit complexity, user experience, and regulatory alignment. Addressing these early prevents costly re-architecting later.

Circuit complexity and cost

Zero-knowledge circuits are computationally expensive. As verification logic grows, proving time and gas costs increase exponentially. This can make real-time KYC checks impractical for high-frequency transactions.

Fix: Modularize your circuits. Break complex identity checks into smaller, reusable proof segments. Use recursive proofs to aggregate multiple verifications into a single on-chain statement, keeping the final verification step lightweight.

User friction and onboarding

If the ZK KYC process requires users to manage multiple keys or wait minutes for proof generation, adoption stalls. Privacy is useless if the user experience is worse than traditional email verification.

Fix: Abstract the cryptography. Use passkeys or biometric authentication on the client side to generate proofs without exposing raw keys. Ensure proof generation happens in the background or via lightweight mobile SDKs, keeping the interface familiar.

Regulatory ambiguity

Regulators may not yet recognize ZK proofs as valid compliance evidence. A proof that you are over 18 is not the same as a government-issued ID check in the eyes of many AML (Anti-Money Laundering) frameworks.

Fix: Partner with licensed KYC providers who can issue "attested" credentials. Your ZK system then verifies the attestation, not the raw identity data. This bridges the gap between decentralized privacy and centralized regulatory requirements.

No comments yet. Be the first to share your thoughts!