How ZK-KYC Systems Work

Traditional Know Your Customer (KYC) processes rely on a risky premise: you must hand over your data to prove who you are. This creates a central repository of sensitive information—passports, bank statements, and proof of residence—that becomes a high-value target for hackers. ZK-KYC flips this model. Instead of storing your personal data, the system generates a cryptographic proof that you meet specific criteria without ever revealing the underlying details.

Imagine you need to prove you are over 21 to enter a club. In the old system, you hand your driver’s license to the bouncer, who sees your name, address, and exact birthdate. With ZK-KYC, you provide a digital signature that simply says "True: Age > 21." The verifier accepts the proof without knowing your name, your address, or even your exact age. This is the core mechanism of Zero-Knowledge Proof KYC.

This shift from data storage to data verification changes the entire security landscape. Because no sensitive personal information is held by the service provider, there is no database to breach. The user retains control of their identity, and the application only receives the binary result of the verification: compliant or not. This approach aligns with privacy-by-default principles, ensuring that regulatory requirements are met without compromising user privacy.

The infrastructure behind this process involves three main actors: the user, the verifier (the application), and the issuer (the trusted KYC provider). The issuer verifies the user’s identity offline or through a secure channel and issues a signed credential. The user then uses this credential to generate a zero-knowledge proof, which they submit to the verifier. The verifier checks the proof against public parameters to confirm validity, all without ever seeing the user’s raw identity data.

By decoupling verification from data storage, ZK-KYC systems offer a more resilient and privacy-preserving alternative to traditional compliance methods. This allows financial institutions and decentralized applications to meet regulatory obligations while respecting user privacy, reducing the risk of data breaches and identity theft.

The Technical Stack Behind ZK KYC Systems

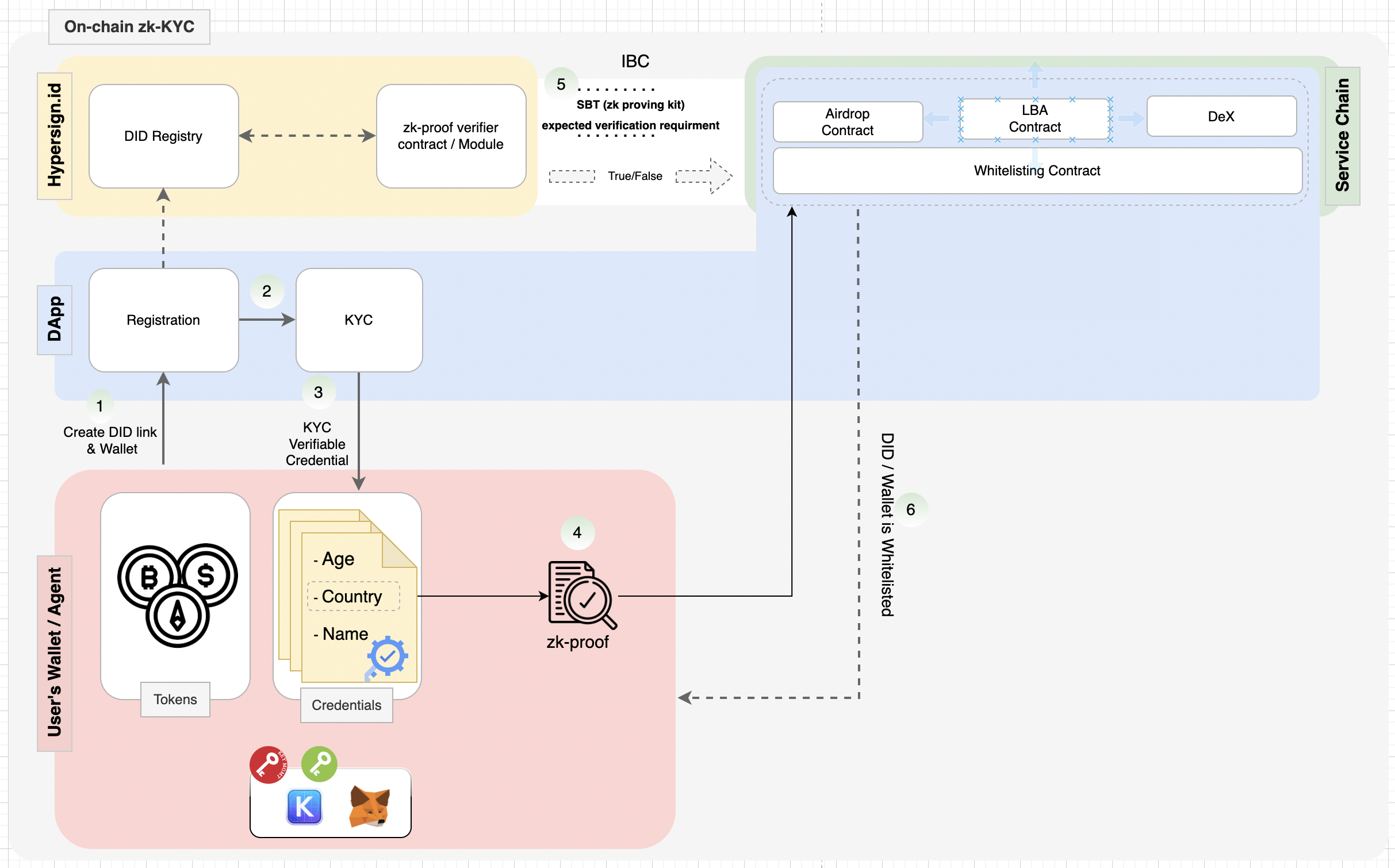

Building a ZK KYC system requires stitching together three distinct layers: the identity verification logic, the zero-knowledge circuit, and the on-chain verifier. This architecture ensures that a user can prove compliance—such as being over 18 or residing in a permitted jurisdiction—without exposing their raw personal data to the dApp or the public blockchain.

Circuit Design and Oracle Integration

The core of the system is the zero-knowledge circuit, often built using frameworks like Circom or SnarkJS. These circuits define the logical rules for validity. For example, a circuit might take a signed attestation from a trusted oracle as input and output a proof that the user’s attributes match the required criteria.

Oracles play a critical role by bridging off-chain identity providers (like government databases or licensed KYC vendors) with the on-chain world. They sign the verification data, ensuring the circuit only accepts proofs from trusted sources. This prevents users from fabricating credentials.

Smart Contract Verification

Once the proof is generated, it is submitted to a smart contract on the target chain. The contract contains the verification logic (the "verifier" contract) that checks the mathematical validity of the ZK proof. If the proof is valid, the contract mints a non-transferable token (like an NFT or Soulbound Token) representing the verified status. This token can then be used by DeFi protocols to grant access without requiring repeated KYC checks.

ZK KYC Systems Market Research

The market for zero-knowledge KYC is moving from experimental pilots to regulated production. The core value proposition is simple: applications verify that a user meets compliance requirements—such as age or jurisdiction—without storing or exposing personal data. This shift is driven by the need to reduce liability from data breaches while satisfying strict regulatory mandates.

Key Players and Capabilities

Three providers currently define the landscape, each with a distinct approach to verification speed and data retention.

| Provider | Verification Speed | Data Retention | Primary Use Case |

|---|---|---|---|

| Treza Labs | Sub-second | None (ZK only) | Crypto & DeFi compliance |

| Zyphe | Sub-second | None | Regulator-grade banking |

| Chainlink | Real-time | Minimal | Oracle-based identity |

Treza Labs focuses on infrastructure for crypto and regulated finance, ensuring that applications can verify compliance without ever touching the underlying documents. Similarly, Zyphe ships regulator-grade verification with sub-second performance, emphasizing that no document retention is necessary for audit trails. Chainlink provides oracle-based identity solutions that integrate with existing Web2 identity providers, bridging the gap between traditional KYC and on-chain verification.

Adoption Trends and Regulatory Drivers

Adoption is accelerating as institutions recognize that storing sensitive PII is a significant liability. A licensed identity provider, such as a government KYC agency, verifies documents once and issues a zero-knowledge proof. The application then verifies this proof without accessing the original data. This model reduces the attack surface for hackers and simplifies compliance with data protection laws like GDPR.

The market is also seeing a convergence of traditional KYC stages with ZK technology. The five standard stages—Customer Identification, Due Diligence, Risk Assessment, Monitoring, and Reporting—are being reimagined. For instance, ongoing monitoring can be performed via periodic ZK proofs rather than continuous data storage. This allows institutions to maintain compliance while minimizing data exposure.

Integrating ZK KYC into Existing Compliance Workflows

Bringing zero-knowledge proof systems into your current compliance stack requires shifting from data collection to data verification. Traditional KYC asks for documents; ZK KYC asks for proofs. This change simplifies the infrastructure but demands careful planning to ensure you meet regulatory standards without compromising user privacy.

The goal is to build a system where users can prove they are compliant—such as being over 18 or not in a sanctioned jurisdiction—without handing over their passport or birth certificate. This approach reduces your liability and aligns with privacy-first design principles.

1. Map Regulatory Requirements to Proof Attributes

Start by listing exactly what your regulators require. You don’t need to prove identity; you need to prove eligibility. Break down each rule into a boolean condition.

- Age Verification: Prove

age >= 18. - Sanctions Screening: Prove

address ∉ OFAC list. - Jurisdiction: Prove

country ∈ allowed_list.

By defining these as discrete attributes, you create a clear blueprint for the zero-knowledge circuit. This ensures your proofs are legally sufficient without being overly broad.

2. Select a Compatible Identity Provider

You need a trusted source that can issue the initial credentials. Choose an identity provider (IdP) that supports zero-knowledge credential issuance. The IdP verifies the user’s real-world identity once and issues a signed credential.

Ensure the IdP supports the cryptographic standards your ZK system uses. This compatibility is critical for generating valid proofs. If the IdP and the verifier don’t speak the same cryptographic language, the system will fail.

3. Design the Circuit

The circuit is the core of your ZK KYC system. It takes the user’s private credential and the public regulatory rules as inputs. It then generates a proof that the rules are met.

Keep the circuit simple. Complex circuits increase verification time and cost. Focus on the specific attributes you need. For example, if you only need to verify age, don’t include jurisdiction checks in the same proof unless necessary.

4. Implement the Verifier on Your Platform

Deploy the verifier smart contract or service on your platform. This component checks the ZK proof generated by the user. If the proof is valid, the user is granted access.

This step should be seamless for the user. They should not need to understand the cryptography. The verifier simply says "yes" or "no" based on the proof. This maintains the privacy-preserving nature of the system while ensuring compliance.

5. Conduct Rigorous Testing

Before launching, test the entire flow with a small group of users. Check for edge cases, such as expired credentials or invalid proofs. Ensure the user experience is smooth and the verification process is fast.

Testing also helps identify any potential security vulnerabilities. ZK systems are complex, and small errors can have big consequences. Make sure your system is robust before going live.

6. Monitor and Update

Regulatory requirements change. Your ZK KYC system must be able to adapt. Set up a monitoring system to track updates to sanctions lists and age requirements.

When rules change, update your circuit and verifier accordingly. This ensures your system remains compliant over time. Regular updates are essential for maintaining trust and legal standing.

Frequently Asked Questions About ZK KYC

How does zk KYC work?

Zero-Knowledge Proof KYC (ZK-KYC) is a privacy-preserving verification method where a user proves they meet specific regulatory criteria—such as age or jurisdiction—to a verifier without revealing underlying personal data. This approach allows compliance teams to confirm identity status while minimizing the exposure of sensitive documents like passports or bank statements, which are traditional targets for data breaches.

What are the 5 stages of KYC?

Traditional KYC processes generally follow five distinct stages to ensure regulatory compliance:

- Customer Identification Program (CIP): Collecting basic identity information.

- Customer Due Diligence (CDD): Verifying the provided information against trusted sources.

- Risk Assessment: Categorizing the customer based on potential money laundering or terrorist financing risks.

- Ongoing Monitoring: Continuously watching transactions for unusual activity.

- Reporting Suspicious Activities: Filing necessary reports with financial authorities when red flags appear.

Does ZK KYC replace traditional KYC?

No, ZK-KYC does not replace the regulatory requirement for identity verification. Instead, it changes how the verification is executed. The underlying legal obligations remain the same, but the technical infrastructure shifts from storing raw personal data to storing cryptographic proofs that satisfy those obligations without exposing the raw data.

Is ZK KYC compliant with GDPR?

Yes, ZK-KYC is often considered more compliant with privacy regulations like GDPR because it adheres to data minimization principles. By only revealing the minimum necessary information to satisfy a specific check (e.g., "over 18" rather than "born on [Date]"), organizations reduce their liability and the potential impact of data leaks.

No comments yet. Be the first to share your thoughts!