The KYC Market and the Rise of Zero Knowledge Proofs

The broader identity verification sector is expanding rapidly, driven by stricter global compliance mandates and the digitization of financial services. According to Mordor Intelligence, the global KYC market is valued at approximately USD 7.8 billion in 2026 and is projected to nearly double, reaching USD 16.31 billion by 2031 with a compound annual growth rate (CAGR) of 15.88% [1]. This growth reflects a baseline demand for identity assurance that is now being reshaped by privacy-preserving technologies.

Within this expanding landscape, zero-knowledge proof (ZKP) systems represent a distinct, high-velocity segment. While traditional KYC relies on sharing extensive personal data with third-party verifiers, ZK KYC allows users to prove eligibility—such as age or residency—without revealing the underlying information. Grand View Research estimates the global zero-knowledge proof market at USD 1.28 billion in 2024, with projections to reach USD 7.59 billion by 2033 [2]. This trajectory suggests that ZK solutions are not just a niche privacy tool but a core infrastructure component for the next generation of compliant identity systems.

The contrast between these two figures highlights a structural shift. As regulatory bodies tighten data protection laws like GDPR and CCPA, the friction of traditional data collection becomes a liability. ZK KYC systems address this by decoupling verification from data storage, aligning with the market's need for both security and user trust.

Figure 1: Performance of Visa Inc. (V) as a proxy for broader identity and payments infrastructure trends. ZK KYC adoption often correlates with increased transaction volume in secure, privacy-compliant digital economies.

This divergence in growth rates indicates that while the total addressable market for KYC is large, the specific segment leveraging zero-knowledge cryptography is capturing value at a faster pace. For legal and regulatory professionals, this signals that ZK infrastructure is moving from experimental pilots to required architectural standards for future-proof compliance.

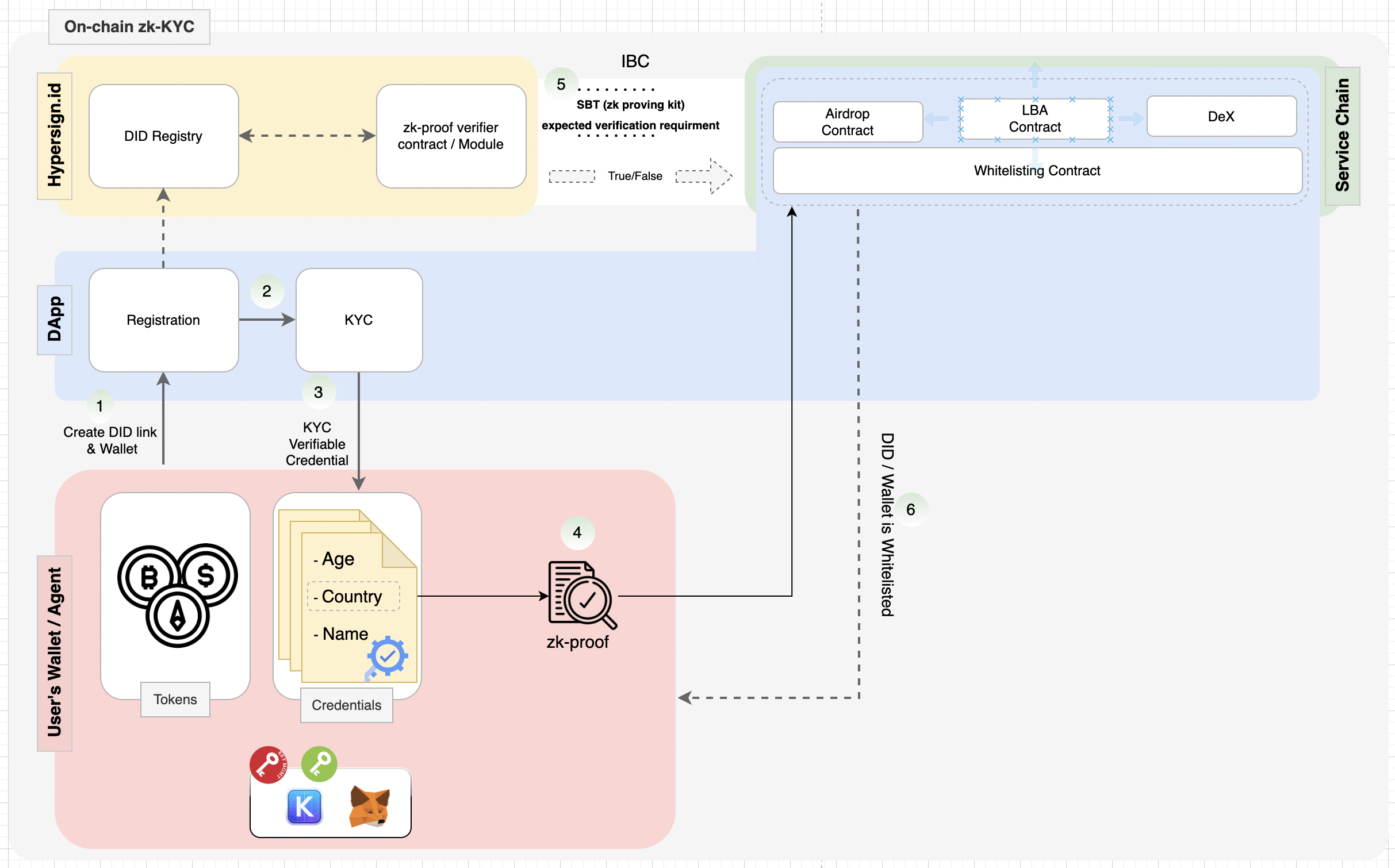

Infrastructure layers in production

A ZK KYC system functions like a secure vault with a specialized window. The infrastructure is built on three distinct layers that work together to verify identity without exposing the underlying data. This separation is the core mechanism that allows financial institutions to meet strict regulatory standards while protecting user privacy.

The first layer is the data ingestion and verification layer. Here, trusted entities—such as government databases, credit bureaus, or identity providers—validate the user’s raw information. This is where the actual check happens: confirming that a passport is genuine or that a person is over 18. This layer does not store the sensitive data; it only processes it to generate a cryptographic proof. The sensitive PII (Personally Identifiable Information) is never retained by the ZK system itself, eliminating the risk of a massive data breach.

The second layer is the zero-knowledge proof generation layer. This is the computational engine that takes the verified data and creates a mathematical proof. Think of this as a sealed envelope. The envelope proves that the contents meet specific criteria (e.g., "Age > 18") without revealing what the contents actually are. This proof is generated on-device or in a secure enclave, ensuring that the raw data never leaves the user’s control or the trusted verifier’s immediate processing environment.

The final layer is the verification and integration layer. This is where the ZK proof is checked by the receiving platform, such as a bank or exchange. The system verifies the cryptographic signature of the proof in milliseconds. If the proof is valid, the platform grants access or compliance status. The platform receives only the "yes" or "no" answer, never the underlying documents. This architecture allows for sub-second verification times and zero document retention, a standard cited by production implementations like Zyphe for its regulatory-grade efficiency.

Competitive landscape and key players

The ZK KYC market is splitting into two distinct camps: legacy identity providers adapting their stacks and native startups building zero-knowledge protocols from the ground up. Traditional players like GB Group and Fenergo are leveraging existing regulatory relationships to integrate ZK proofs into established workflows, while newer entrants focus on privacy-first architectures for decentralized finance (DeFi) and institutional compliance. This divergence creates a fragmented but rapidly evolving ecosystem where trust is distributed rather than centralized.

According to recent market analysis, the broader KYC market is projected to reach USD 7.8 billion in 2026, growing at a CAGR of 15.88% through 2031. This growth is driven by the urgent need for systems that satisfy regulatory scrutiny without exposing raw personal data. The separation of duties in ZK architectures allows institutions to verify compliance without holding sensitive keys, a shift that is redefining competitive advantages in the sector.

The table below contrasts the primary approaches of major market participants, highlighting their technological focus and target regulatory environments.

| Provider | ZK Approach | Primary Focus | Regulatory Fit |

|---|---|---|---|

| GB Group | Hybrid integration | Enterprise KYC/AML | Traditional banking |

| Fenergo | Modular ZK modules | Risk & Compliance | Global financials |

| Studio AM | Native ZK protocols | Institutional DeFi | Crypto-adjacent |

| ZK Labs (Hypothetical) | Full-stack ZK | Privacy-first identity | GDPR/CCPA |

Strategic adoption in regulated sectors

Zero-knowledge KYC systems are moving from experimental prototypes to core infrastructure in sectors where privacy and compliance collide. The strategic value lies in separating identity verification from transactional data, allowing platforms to prove regulatory adherence without exposing sensitive user details.

In decentralized finance, this separation is critical. Traditional KYC requires sharing full identity documents with centralized entities, creating single points of failure for data breaches. ZK-KYC distributes trust across multiple actors, ensuring no single entity holds all the keys to user identity. This structure allows DeFi platforms to onboard institutional capital that demands strict compliance while preserving the privacy principles that define the sector.

Traditional finance is also integrating these systems to streamline cross-border transactions. By using zero-knowledge proofs, banks can verify a customer’s eligibility for specific financial products without transmitting raw personal data between institutions. This reduces regulatory overhead and minimizes the risk of data leakage during inter-bank settlements.

Gaming and metaverse platforms face similar pressures. As virtual economies grow, anti-money laundering regulations require identity verification for high-value transactions. ZK-KYC allows players to prove they are of legal age or reside in permitted jurisdictions without revealing their real-world identity to game developers or other players. This balance enables mass adoption while satisfying regulatory requirements.

The trade-off is clear: platforms must invest in robust cryptographic infrastructure to maintain these proofs. However, the long-term benefit is a compliance framework that scales with user growth without compromising security or privacy.

Regulatory drivers and compliance

The regulatory landscape for zero-knowledge KYC is defined by a tension between privacy mandates and anti-money laundering requirements. ZK systems provide defensibility against per-decision compliance tests by separating identity verification from transactional data. This architecture allows institutions to satisfy eIDAS 2 and AML directives without retaining sensitive personal information.

The European Union’s eIDAS 2 regulation establishes a framework for digital identity that aligns with ZK principles. By enabling users to prove attributes without revealing underlying data, ZK KYC supports the EU’s goal of secure, privacy-preserving digital interactions. This alignment reduces regulatory friction for financial institutions operating across borders.

Anti-money laundering directives require financial entities to verify customer identities and monitor transactions. ZK systems address these requirements by providing cryptographic proof of compliance. Institutions can demonstrate that a user meets regulatory criteria without exposing their full identity profile. This approach minimizes data breach risks while maintaining auditability.

The separation of duties in ZK KYC distributes trust across multiple actors. No single entity holds all the keys to user data, reducing the impact of potential breaches. This distributed trust model is particularly valuable in decentralized finance, where traditional centralized verification methods are less effective.

ZK KYC solutions offer regulator-grade verification with sub-second performance. They enable compliance without document retention, addressing concerns about data storage and liability. This capability is critical for institutions seeking to balance regulatory compliance with user privacy.

Institutional adoption of ZK KYC is driven by the need for scalable, privacy-preserving compliance. As regulations evolve, ZK systems provide a flexible infrastructure that can adapt to new requirements. This adaptability makes ZK KYC a strategic investment for financial institutions navigating the complex regulatory environment.

Frequently asked questions about ZK KYC systems

How fast are zero-knowledge KYC verifications?

ZK proofs enable near-instant identity checks by generating cryptographic evidence of compliance without reprocessing raw data. Production systems like Zyphe demonstrate sub-second verification speeds, allowing platforms to approve users in real time without the latency of manual review or traditional database lookups [src-serp-3].

Do companies retain user documents under ZK KYC?

No. The core advantage of ZK-KYC is that the service provider never stores or sees the underlying identity documents. Users generate a proof that they meet specific criteria, such as being over 18 or residing in a permitted jurisdiction, and the verifier accepts the proof without retaining the source data [src-serp-5].

Is ZK KYC accepted by regulators?

Regulatory acceptance is growing but remains nuanced. While ZK proofs satisfy privacy-preserving compliance goals, regulators still require a trusted onboarding step to link the cryptographic identity to a real-world person. Most current frameworks rely on a "trusted setup" or initial vetting by a licensed entity before ZK proofs are used for ongoing transactions [src-serp-5].

No comments yet. Be the first to share your thoughts!