Why traditional KYC fails Web3

Traditional KYC processes were built for a centralized world, not a decentralized one. In the legacy financial system, handing over a passport or driver's license to a bank makes sense because the bank is a single, accountable entity. In Web3, that same model creates a massive single point of failure. When you upload your identity documents to a centralized server, you are creating a honeypot for hackers. The history of data breaches in centralized finance is long and well-documented, making the risk of identity theft an unacceptable cost for users who value privacy.

Beyond security, traditional KYC violates the core ethos of decentralized finance: self-sovereignty. Centralized providers often store data indefinitely, creating permanent records that can be subpoenaed, sold, or leaked. This lack of data minimization means that every interaction with a compliant platform leaves a digital footprint that can be traced back to your real-world identity. For many Web3 participants, this loss of anonymity is not just a privacy concern but a fundamental incompatibility with the technology they are using.

This structural flaw is why the industry is turning toward Zero-Knowledge KYC. Instead of storing your actual documents, ZK-KYC systems verify that you meet compliance requirements—such as being over 18 or not being on a sanctions list—without ever exposing the underlying personal data. This approach aligns regulatory compliance with the privacy-preserving nature of blockchain, removing the central repository that makes traditional KYC so vulnerable.

How ZK proofs verify identity

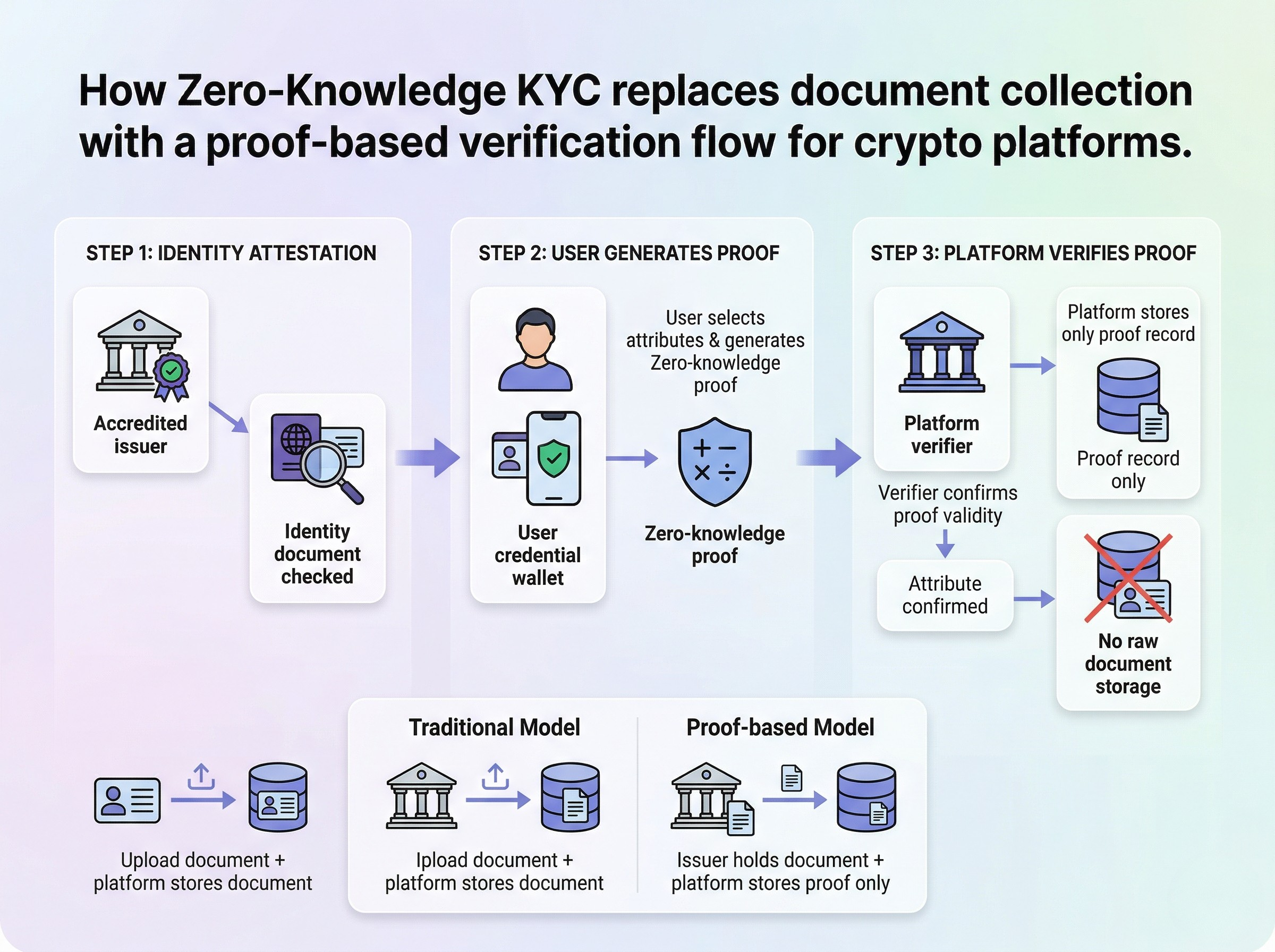

Zero-knowledge proofs (ZKPs) allow a system to verify that a user meets specific identity criteria without exposing the underlying personal data. In a ZK-KYC framework, the goal is binary: prove compliance or fail, while keeping the raw documents—passports, selfies, and addresses—completely hidden from the verifier.

The process begins with a trusted setup, where cryptographic parameters are generated to create a "proof system." This system defines the rules for what constitutes valid identity. For example, the circuit might be programmed to accept only inputs that match a specific government-issued ID format and confirm the holder is over 18. Once the circuit is established, the user’s data is hashed and processed within this mathematical structure.

The user’s device, or a dedicated identity provider, generates a cryptographic proof. This proof is a short string of data that mathematically demonstrates the input satisfied the circuit’s constraints. Crucially, this proof contains no information about the input itself. It is akin to proving you have a valid key to a lock without showing the key’s shape or the lock’s internal mechanism.

When the service chain receives this proof, it runs a verification algorithm. This step is computationally cheap and fast, often taking milliseconds. The verifier checks the proof against the public parameters of the circuit. If the proof is valid, the system outputs a simple "true" signal, granting access or completing the transaction. The original personal data never touches the blockchain or the service provider’s servers, eliminating the risk of a centralized database breach exposing user identities.

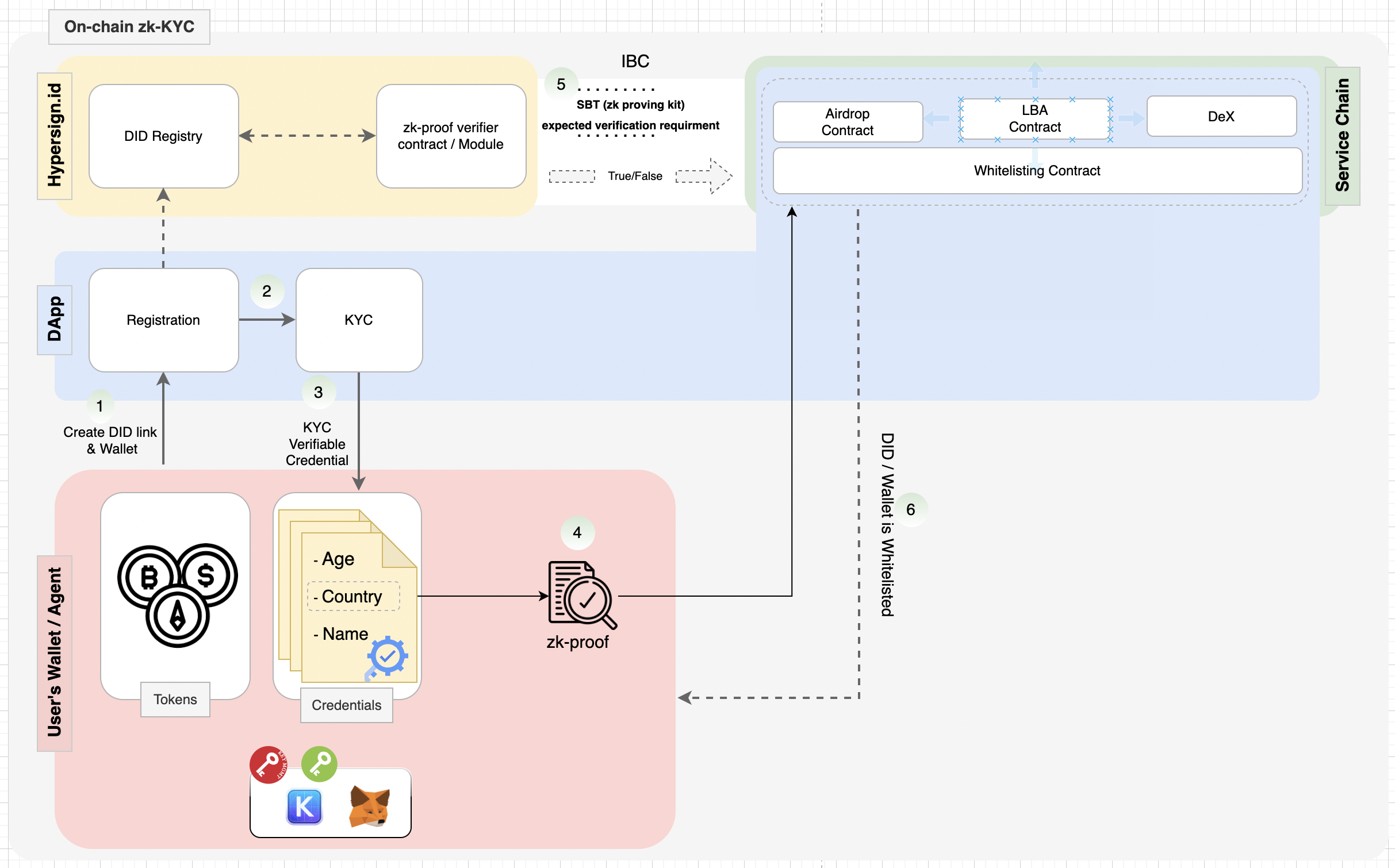

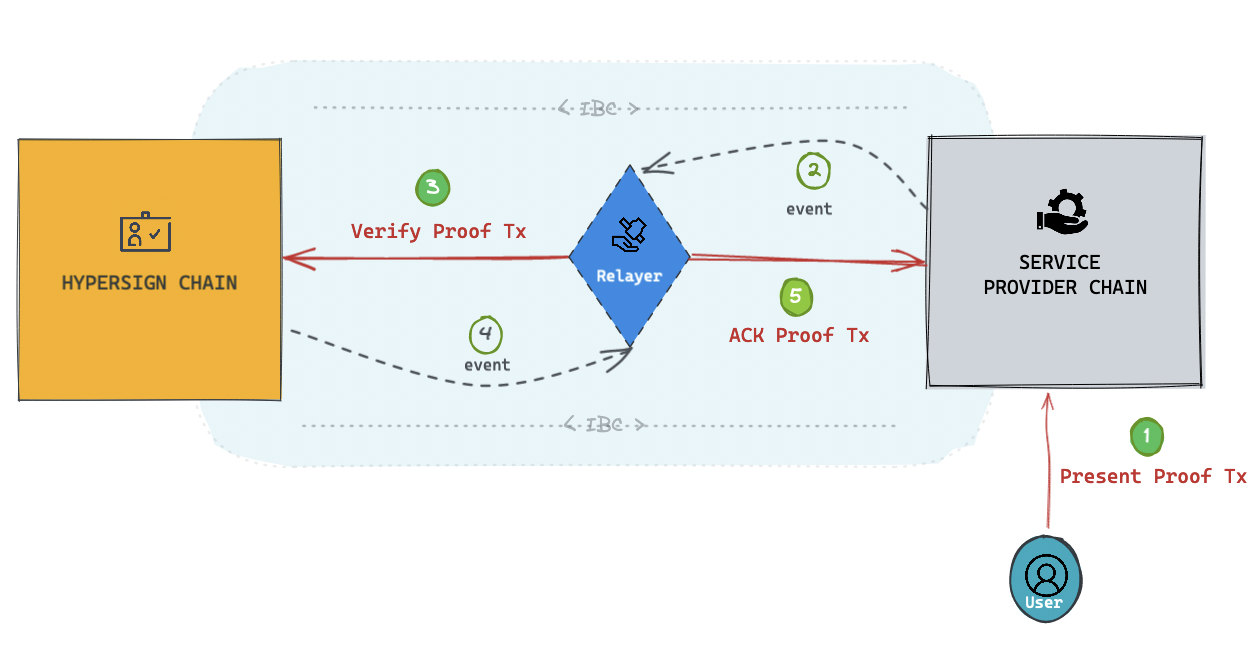

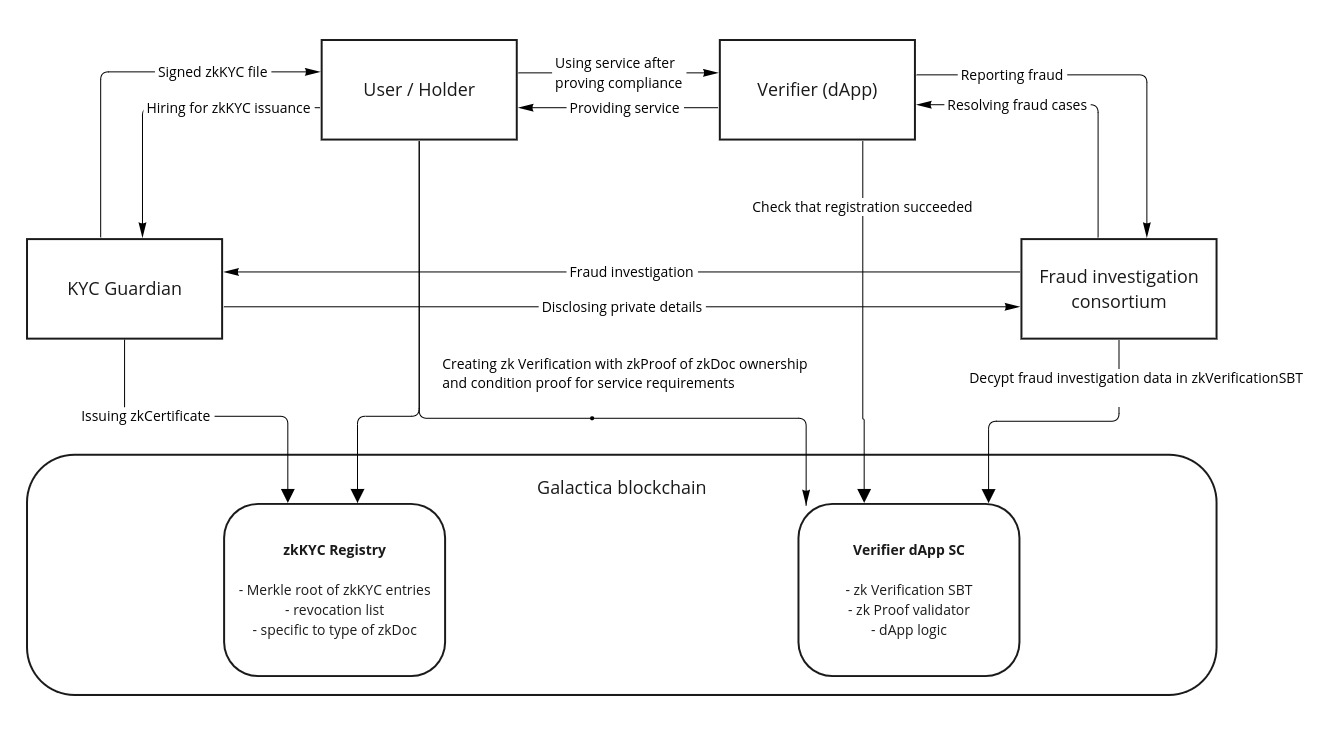

Key infrastructure components

Market adoption and regulatory fit

Institutional adoption of ZK KYC is moving from pilot programs to core infrastructure. As regulatory pressure mounts, DeFi protocols are integrating zero-knowledge proofs to satisfy compliance without exposing user data. This shift allows institutions to operate within decentralized finance while adhering to strict anti-money laundering (AML) and know-your-customer (KYC) mandates.

The architecture typically separates the verification layer from the service chain. Identity systems issue zero-knowledge credentials that prove a user’s status—such as being accredited or geographically compliant—without revealing the underlying personal information. This separation enables DeFi applications to query identity status efficiently while maintaining user privacy.

Global regulations are evolving to accommodate these technologies. Frameworks in the EU and Asia are increasingly recognizing zero-knowledge proofs as a valid method for data minimization. This legal alignment reduces the friction for institutional players who previously avoided DeFi due to compliance uncertainty. As standards solidify, ZK KYC is becoming a prerequisite for mainstream financial integration.

Building a ZK KYC strategy

Implementing zero-knowledge KYC requires balancing regulatory compliance with user privacy. Projects must move beyond abstract concepts to build infrastructure that satisfies auditors while keeping onboarding friction low. The goal is to verify eligibility without storing sensitive personal data on-chain or in centralized databases.

By following these steps, you create a robust ZK KYC infrastructure. This approach ensures that your project meets legal standards while respecting user privacy, a critical factor for adoption in decentralized finance.

Common zk kyc: what to check next

Zero-knowledge proof (ZKP) systems introduce new mechanics for identity verification, which naturally raises questions about privacy, control, and regulatory acceptance. Below are answers to the most frequent concerns regarding how these systems handle sensitive data and compliance.

The core challenge lies in balancing privacy with the legal obligation to identify users. As noted in industry analyses, designing these systems requires avoiding "master keys" that could compromise the entire identity infrastructure while still allowing for necessary compliance checks. This approach ensures that privacy is preserved by default, but only within the bounds of legal verification.

No comments yet. Be the first to share your thoughts!