How ZK KYC systems verify identity

Zero-Knowledge Proof KYC (ZK-KYC) is a privacy-preserving verification method where a user proves they meet specific regulatory criteria—such as age or jurisdiction—to a verifier without revealing underlying personal data. Traditional KYC requires you to hand over your passport, selfie, and address proof to a centralized database. ZK-KYC flips this model. Instead of sharing the data itself, you share a cryptographic proof that the data exists and is valid.

Think of it like a nightclub bouncer. In the old system, you hand over your ID, and the bouncer reads your name, address, and birthdate, then keeps a copy of that ID in a filing cabinet. In a ZK-KYC system, you prove you are over 21 without ever showing your name or birthdate. The bouncer gets a simple "yes" or "no" signal. The underlying personal details remain hidden, even from the platform verifying you.

This mechanism relies on zero-knowledge proofs, a form of cryptography that allows one party to prove to another that a statement is true without revealing any information beyond the validity of the statement itself. For compliance, this means an application can verify that a user is not on a sanctions list, is over the legal age, or resides in an allowed jurisdiction, all without storing sensitive identity documents. As noted by Treza Labs, ZK-KYC allows applications to verify that a user meets compliance requirements without exposing or storing personal data.

The result is a system that satisfies regulators who demand verification while protecting users from the massive data breaches that have plagued traditional centralized KYC providers. You prove your eligibility, but you keep your identity private.

Infrastructure layers in ZK KYC

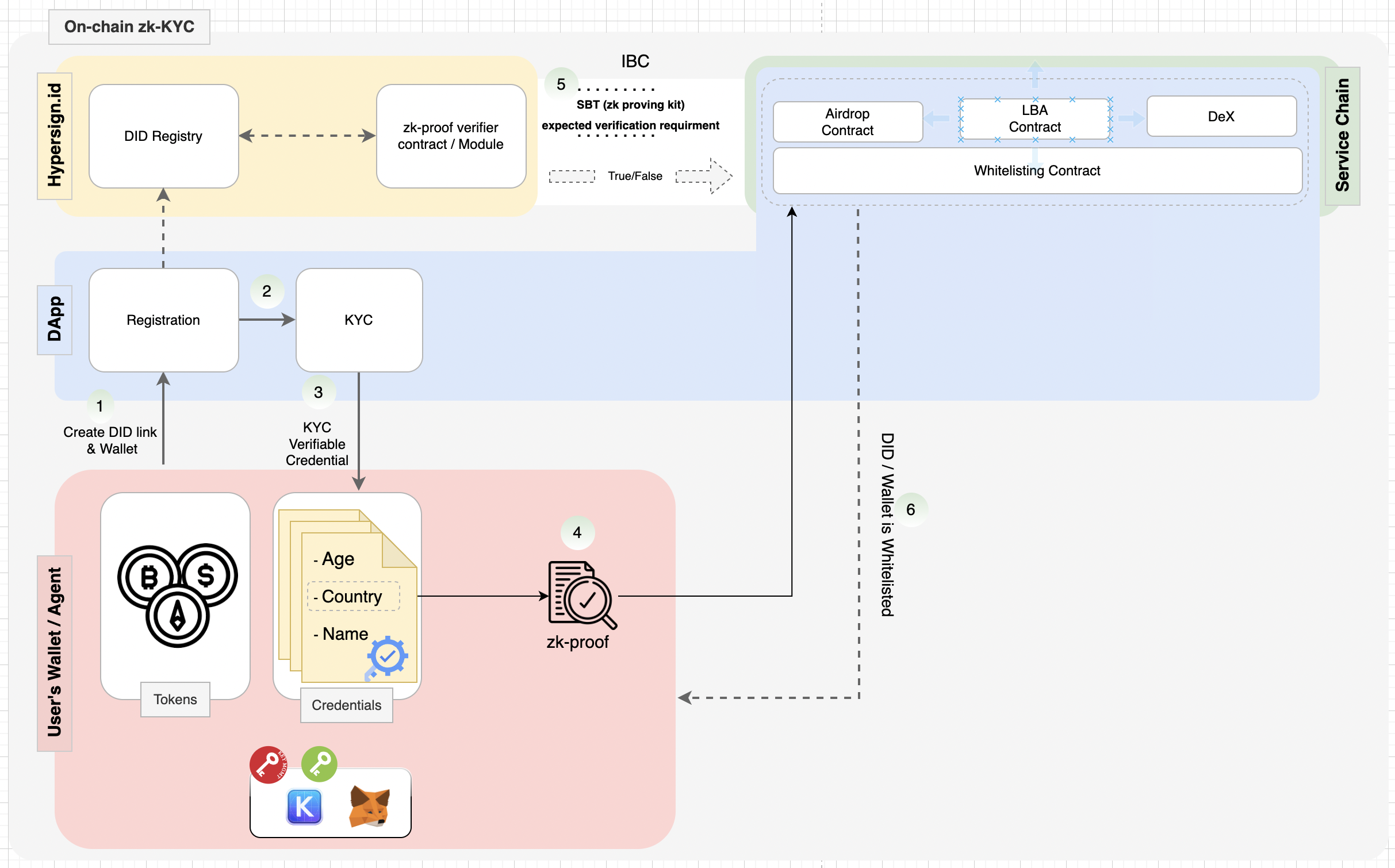

Building a ZK KYC system requires separating identity from verification. The architecture typically splits into three distinct layers: Identity Providers (IPs), ZK Circuits, and Verifiers. This separation ensures that no single entity holds the complete picture of a user’s identity, preventing the central data silos that plague traditional compliance models.

Identity Providers act as the trusted origin of truth. These are established entities like government agencies, certified banks, or licensed KYC vendors. They hold the raw personal data—passports, facial scans, and address proofs. In a ZK KYC flow, the IP does not send this data to every service. Instead, it issues a signed credential or a private key that proves the user’s attributes. Think of the IP as a notary: they verify the document but don’t keep a copy for every person who sees it.

The ZK Circuit is the computational engine that transforms these credentials into proofs. This is where the heavy lifting happens. The circuit takes the user’s private data and a set of public rules (e.g., "must be over 18" or "must not be in a sanctioned country") and generates a zero-knowledge proof. This proof is a cryptographic snippet that confirms the user meets the criteria without revealing the underlying data. The circuit ensures that the verification is mathematically sound and privacy-preserving.

Verifiers are the final checkpoint, usually deployed as smart contracts on a blockchain. When a user wants to access a DeFi protocol or a regulated service, they submit the ZK proof to the verifier. The contract checks the proof against the circuit’s rules. If the proof is valid, the verifier grants access. The verifier never sees the user’s name, ID number, or address. It only sees the proof and the result: true or false.

This layered approach solves the redundancy problem highlighted by providers like zkPass, where users repeat the same KYC process across multiple platforms. By decoupling the identity source from the verification mechanism, ZK KYC allows a single verification event to be reused across different services. The identity provider issues the credential once, the user generates the proof once, and any verifier can accept it. This creates a modular infrastructure where compliance is a service, not a siloed database.

Market strategy for ZK KYC adoption

The push for Zero-Knowledge Proof (ZK) KYC systems is no longer just a privacy preference; it is becoming a regulatory and operational necessity. Traditional KYC models, which require users to upload sensitive documents to centralized servers, create massive liability. When institutions adopt ZK KYC, they shift from storing data to verifying proofs, significantly reducing the attack surface for breaches.

Regulatory Pressure and Institutional Needs

Regulators are tightening compliance frameworks. The EU’s Markets in Crypto-Assets (MiCA) regulation and the Financial Action Task Force (FATF) guidelines demand robust identity verification. However, they also emphasize data minimization. ZK KYC aligns with these goals by allowing users to prove they meet criteria—such as being over 18 or located in a permitted jurisdiction—without revealing their actual identity or location data.

Institutional DeFi platforms are adopting this approach to mitigate risk. By using zero-knowledge proofs, these platforms can ensure compliance without holding a honeypot of user data. This privacy-preserving compliance model attracts users who are wary of traditional data collection practices, giving early adopters a competitive edge in a crowded market.

Comparing Verification Models

The shift from traditional to ZK-based verification changes the risk profile for both users and providers. The table below highlights the core differences in data handling and security.

| Feature | Traditional KYC | ZK KYC |

|---|---|---|

| Data Storage | Centralized database | Zero (proofs only) |

| Breach Risk | High (full PII exposed) | Low (no PII stored) |

| User Privacy | Minimal | Maximum |

| Verification Speed | Minutes to days | Sub-second |

Market Implications

The market for ZK KYC is growing as institutions seek to balance compliance with user trust. Platforms that implement these systems can offer faster onboarding and stronger security guarantees. This strategic advantage is becoming a key differentiator in the crypto and fintech sectors.

Compliance strategy for regulated DeFi

The core tension in decentralized finance is balancing regulatory adherence with user privacy. ZK KYC resolves this by allowing users to prove they meet specific legal criteria—such as not being on a sanctions list or being of legal age—without exposing their underlying identity data. This "lawful intercept" model ensures that compliance officers can verify eligibility without creating a centralized database of sensitive personal information that could be hacked or misused.

1. Verify Regulatory Criteria Without Raw Data

The first step is defining which regulatory thresholds matter for your protocol. Instead of storing a user’s passport or government ID, the system generates a zero-knowledge proof that confirms the user satisfies the condition. For example, a proof can confirm a user is over 18 or resides in a non-sanctioned jurisdiction without revealing their birthdate or exact address. This approach aligns with the Travel Rule and other anti-money laundering (AML) frameworks by providing auditability without data leakage.

2. Implement Sanctions Screening via ZK Proofs

Sanctions screening requires checking user identities against government lists (like OFAC). In a ZK KYC system, the user generates a proof that their identity hash does not match any entry on the blocked list. The verifier (the DeFi protocol) accepts this proof as evidence of compliance. This prevents the protocol from ever seeing the user’s actual identity, reducing liability and protecting user privacy while still satisfying regulatory screening requirements.

3. Design a Privacy-Preserving Verifier

The verifier must be designed to accept ZK proofs without acting as a data broker. This often involves a dedicated identity layer or "Service Chain" that handles the verification logic separately from the main DeFi application. The protocol interacts with this layer to request proofs, and the user presents them when accessing services. This separation ensures that no single entity holds a master key or a comprehensive database of user identities, mitigating the risk of large-scale data breaches.

4. Ensure Ongoing Compliance Monitoring

Compliance is not a one-time check. ZK KYC systems must support ongoing monitoring, such as re-verifying sanctions status or updating risk assessments. Users can generate new proofs periodically or when triggered by specific events (like a large transaction). This ensures that compliance remains current without requiring constant re-submission of personal documents, maintaining a seamless user experience while adhering to regulatory standards.

5. Audit and Transparency

Finally, the system must provide transparent audit trails for regulators. While user data remains private, the protocol can log that a valid ZK proof was presented and accepted. This allows regulators to verify that the protocol is enforcing compliance rules without accessing the underlying personal data. This balance of transparency and privacy is essential for building trust with both users and regulatory bodies.

ZK KYC Systems Guide FAQ

How does ZK KYC work?

Zero-Knowledge Proof KYC (ZK-KYC) allows a user to prove they meet specific regulatory criteria—such as age or jurisdiction—without revealing underlying personal data. This privacy-preserving method ensures compliance while keeping sensitive identity information hidden from the verifier [source 1].

What are the 5 stages of KYC?

Standard KYC procedures follow five distinct stages: Customer Identification Program (CIP), Customer Due Diligence (CDD), Risk Assessment, Ongoing Monitoring, and Reporting Suspicious Activities. ZK systems typically automate the verification steps within this framework to maintain efficiency [source 2].

Is it illegal to buy crypto without KYC?

Buying crypto without verification is legal in most jurisdictions, though tax obligations still apply regardless of the purchase method. However, financial institutions and regulated exchanges are increasingly mandated to enforce KYC protocols to align with international anti-money laundering regulations [source 3].

No comments yet. Be the first to share your thoughts!