Why traditional KYC breaks down

Traditional KYC processes rely on a centralized model that simply does not scale for the modern digital economy. When a user verifies their identity with one platform, that entity stores the sensitive personal data—often including government IDs and biometric information—in its own database. This creates a fragmented landscape where users must repeat the same arduous verification process across multiple services, leading to redundant efforts and heightened friction. For enterprises, this means bearing duplicated compliance costs for every new partnership or user acquisition channel.

The security implications of this siloed approach are severe. Centralized databases are prime targets for cyberattacks, making them attractive targets for bad actors seeking to steal personally identifiable information (PII). A single breach at one identity provider can expose millions of users’ sensitive data, undermining trust and triggering significant regulatory penalties. The concentration of data amplifies the risk, turning every platform into a potential liability.

Regulatory Risk: Storing PII in centralized databases increases exposure to data breaches and regulatory non-compliance, particularly under frameworks like GDPR and CCPA.

The lack of interoperability between these isolated systems creates inefficiencies that stifle innovation. Users cannot easily share verified credentials with new platforms without undergoing full re-verification. This bottleneck slows down user onboarding and increases abandonment rates. Zero-knowledge KYC addresses these structural flaws by decoupling verification from storage, allowing users to prove compliance without exposing their underlying data to every third party they interact with.

How ZK KYC Infrastructure Works

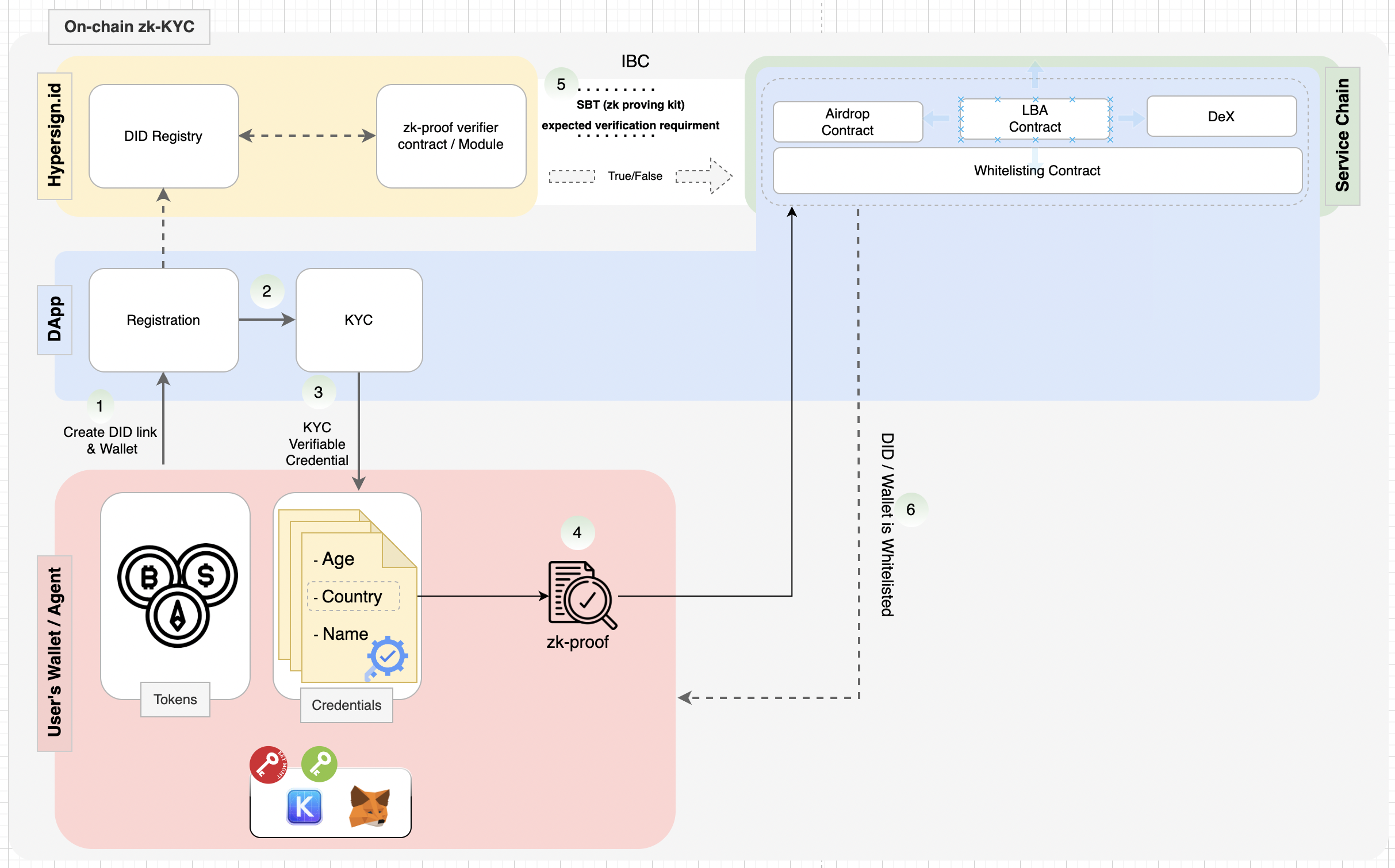

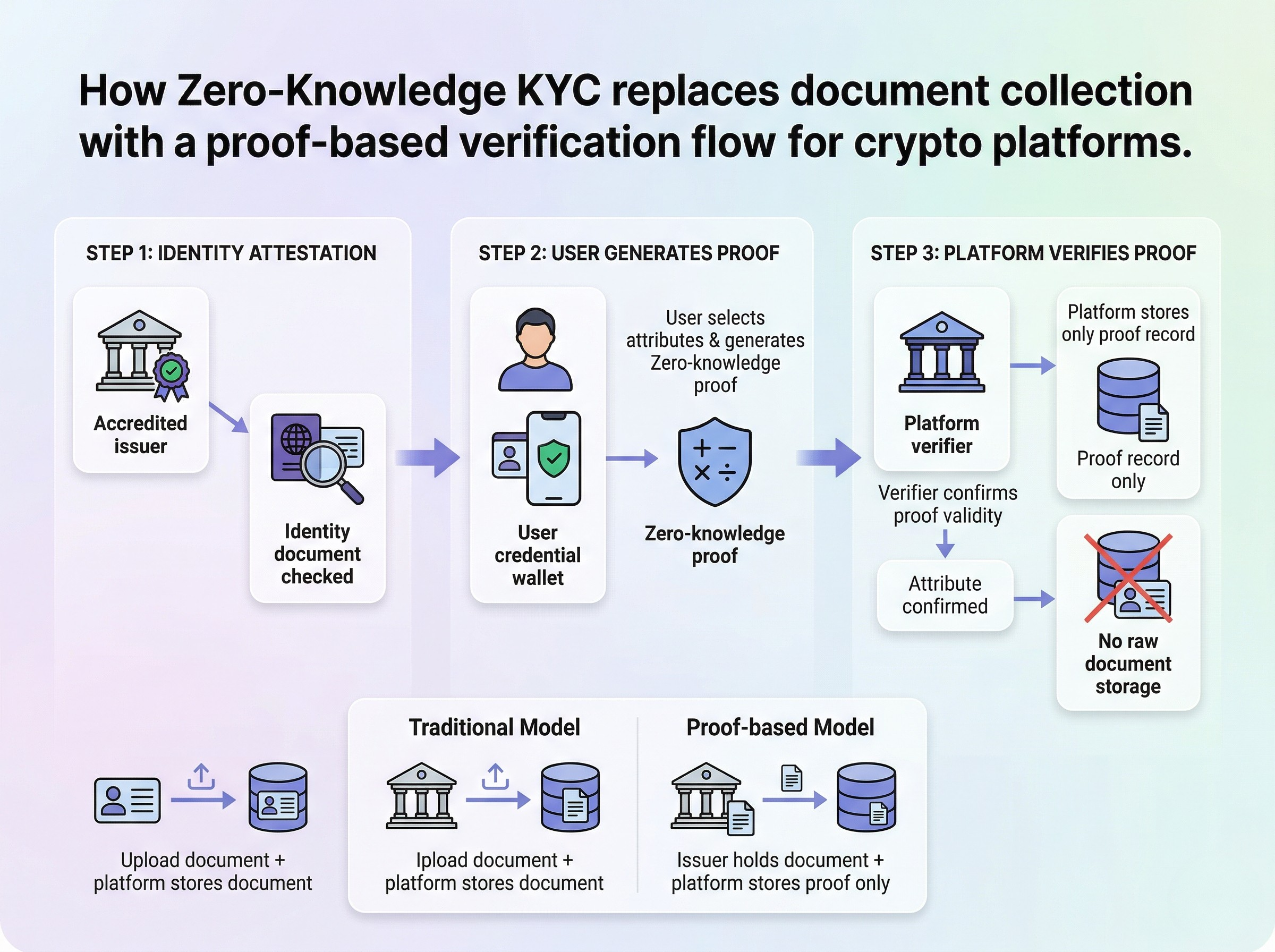

The architecture of Zero-Knowledge KYC (ZK-KYC) functions like a secure, one-time verification gate. Instead of submitting sensitive documents to every service provider, a user interacts with a trusted Identity Provider once. This provider verifies the user’s credentials against regulatory standards and then issues a cryptographic proof. Applications can then verify this proof instantly without ever seeing the underlying personal data.

1. Initial Identity Verification

The process begins when a user submits identity documents—such as a passport or driver’s license—to a trusted Identity Provider. This entity performs a Know Your Customer (KYC) check, validating the user’s age, jurisdiction, and legal status. Unlike traditional systems that store these documents in databases, the Identity Provider’s role is limited to this initial verification. Once confirmed, the provider moves to the next phase: generating a cryptographic credential.

2. Generating the Zero-Knowledge Proof

After verification, the Identity Provider creates a zero-knowledge proof (ZKP). This mathematical artifact confirms that the user meets specific criteria—such as being over 18 or residing in a permitted jurisdiction—without revealing the actual data. The proof is cryptographically signed by the Identity Provider, establishing its trustworthiness. This step is critical because it decouples the verification of facts from the exposure of those facts. The user now holds a portable credential that can be used across multiple services.

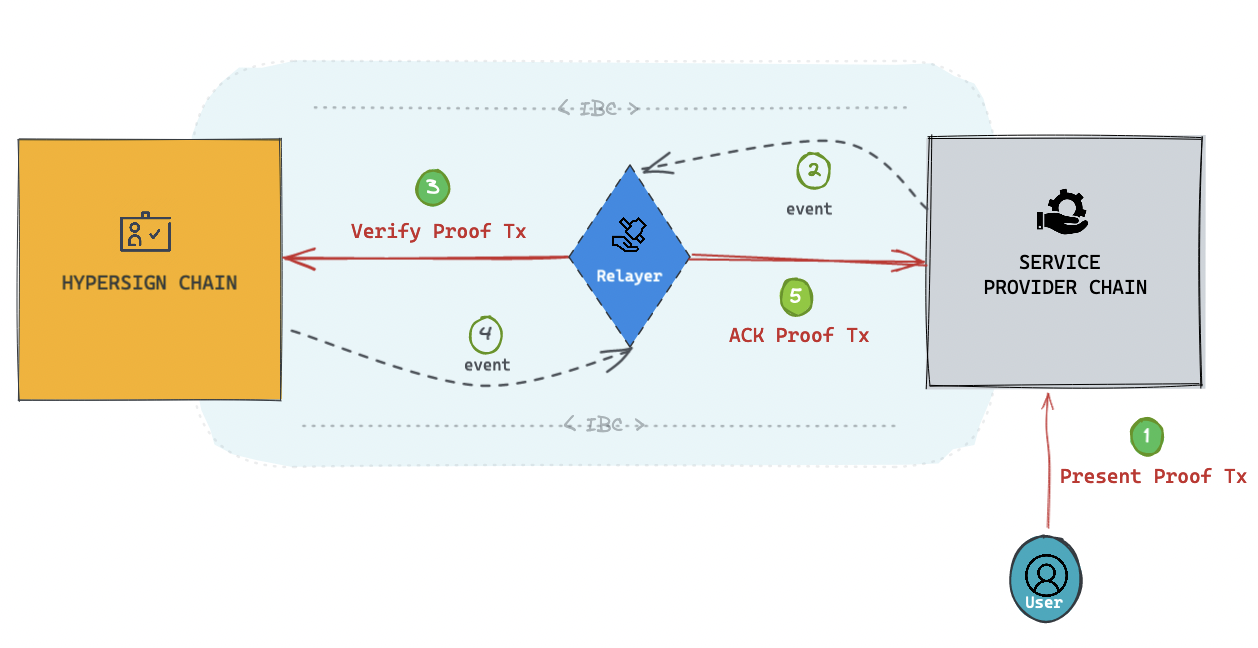

3. Verifying Claims on the Service Chain

When a user interacts with a decentralized application or financial service, they present the ZKP rather than their documents. The application, often running on a separate "Service Chain," verifies the proof against the Identity Provider’s public key. This verification is fast and automated, confirming compliance without storing any personal information. The service gains the necessary assurance to allow access while maintaining the user’s privacy. This flow ensures that data minimization is built into the infrastructure, not just an afterthought.

Compliance frameworks and legal readiness

ZK KYC Systems works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Market leaders and infrastructure providers

The ZK KYC market is shifting from experimental protocols to production-grade infrastructure. Providers are no longer just demonstrating zero-knowledge proofs in isolation; they are building the middleware that allows decentralized applications to verify compliance without storing sensitive user data. This distinction separates legacy KYC aggregators from next-generation privacy layers.

Treza Labs: Institutional-Grade Verification

Treza Labs focuses on the intersection of regulated finance and crypto, offering infrastructure that allows applications to verify user eligibility without exposing personal identifiable information (PII). Their architecture is designed for high-stakes environments where regulatory audit trails are mandatory but data minimization is required. By decoupling the verification logic from the user's identity, Treza enables platforms to onboard users across borders while maintaining strict compliance standards.

zkPass: Browser-Based Data Verification

zkPass takes a different approach by leveraging browser-based zero-knowledge proofs to verify off-chain data. Instead of relying solely on on-chain attestations, zkPass allows users to prove the validity of external documents—such as bank statements or government IDs—directly from their browser. This method addresses the redundancy of users repeating KYC processes across multiple platforms, allowing enterprises to accept verified claims without duplicating the heavy lifting of document collection and storage.

Zyphe: Sub-Second Regulatory Compliance

Zyphe prioritizes performance and user experience, aiming to ship regulator-grade verification with sub-second latency. In a market where friction kills adoption, Zyphe’s solution ensures that privacy-preserving checks do not become a bottleneck. Their system is built to handle high-volume transactions without retaining user documents, offering a streamlined path for DeFi protocols and AI applications that need to verify user credentials in real-time.

Choosing a ZK KYC Provider for Your Stack

Selecting a ZK KYC provider requires balancing technical capability with regulatory reality. You are not just buying software; you are integrating a compliance layer that must withstand legal scrutiny while remaining invisible to the end user.

Ensure the provider supports the specific zero-knowledge predicates your application needs, such as age verification, jurisdiction whitelisting, or sanction screening. If your protocol requires proving a user is not from a sanctioned country, the provider must support that exact logical constraint out of the box.

The provider must comply with relevant data protection laws like GDPR and CCPA. Since they hold the underlying identity data, their security posture is your liability. Request their audit reports and SOC 2 certifications to verify how they store and process sensitive personal information.

ZK proof generation can be computationally expensive. Measure the time from user submission to proof verification on-chain. High latency creates friction and increases dropout rates. Look for providers offering pre-computed proofs or hardware acceleration to keep transaction times under a few seconds.

-

Audit provider security certifications (SOC 2, ISO 27001)

-

Confirm support for required predicates (age, jurisdiction, sanctions)

-

Test proof generation latency under load

-

Review data retention and deletion policies

-

Verify on-chain verifier contract compatibility

Focus on providers with clear documentation and active developer support. The best ZK KYC system is one that integrates seamlessly into your existing stack without requiring custom cryptographic engineering.

Frequently asked questions about ZK KYC

Zero-Knowledge Proof KYC (ZK-KYC) is a privacy-preserving verification method where a user proves they meet specific regulatory criteria—such as age or jurisdiction—to a verifier without revealing underlying personal data source.

How does ZK-KYC work?

ZK-KYC works by generating a cryptographic proof that attests to the validity of your credentials without exposing the raw data itself. Instead of uploading your passport or driver's license to a central database, your wallet or identity provider creates a mathematical proof that you are over 18 or reside in a permitted jurisdiction. The verifier checks this proof against public parameters to confirm it is valid, ensuring the system knows you are compliant without ever seeing your actual identity documents.

Is ZK-KYC fully decentralized?

Current implementations often rely on a trusted issuer, such as a government agency or certified identity provider, to initially verify and sign your credentials. While the verification of the proof can be decentralized on a blockchain, the initial "on-ramp" of trust typically remains centralized. True decentralization requires a distributed web of trust, which is still evolving. The challenge lies in establishing a secure mechanism to verify the initial identity without creating a single point of failure or surveillance risk.

Can ZK-KYC replace traditional KYC?

ZK-KYC is designed to complement, not necessarily replace, existing frameworks in the short term. It offers a superior privacy layer for digital asset services and DeFi protocols, allowing them to comply with regulations like the Travel Rule without storing sensitive user data. However, regulatory acceptance is still growing. Many institutions view it as a future-proof infrastructure upgrade rather than an immediate standalone replacement for legacy systems.

No comments yet. Be the first to share your thoughts!