What zero-knowledge KYC actually means

Zero-knowledge KYC (zKYC) is a privacy-preserving verification method that replaces data hoarding with cryptographic proof. Instead of requiring users to upload passports, selfies, and utility bills to a central database, zKYC allows applications to verify that a user meets specific compliance requirements without exposing or storing any personal data.

This approach shifts the compliance model from data storage to data minimization. The system generates a cryptographic proof that confirms an attribute—such as "over 18" or "not on a sanctions list"—is true. The underlying personally identifiable information (PII) remains with the user or a trusted issuer, never touching the verifier’s infrastructure.

For financial institutions and regulated entities, this creates a new paradigm for balancing regulatory compliance and user privacy in decentralized finance. It eliminates the risk of large-scale data breaches exposing sensitive customer information, which has become a primary liability in traditional identity verification systems.

Market size and growth drivers in 2026

The financial trajectory for identity verification infrastructure is shifting from legacy compliance to cryptographic privacy. The broader KYC market is projected to reach USD 7.8 billion in 2026, growing at a compound annual growth rate (CAGR) of 15.88% through 2031 [[src-serp-1]]. This expansion is driven by stricter global regulatory frameworks and the increasing need for financial institutions to reduce fraud without compromising user data.

Simultaneously, the underlying zero-knowledge proof (ZK) technology is accelerating faster than the general KYC sector. Valued at $3.4 billion in 2025, the ZK market is expected to reach $23.7 billion by 2034, reflecting a robust CAGR of 24.1% [[src-serp-4]]. This divergence highlights a clear industry pivot: organizations are moving beyond basic data collection toward systems that utilize cryptographic proof and data minimization to verify identity without exposing sensitive personal information.

This growth is not limited to traditional banking. The shift toward Web3 and DeFi adoption is creating new demand for ZK KYC systems that can bridge regulated finance with decentralized protocols. As identity verification becomes a foundational layer for digital trust, the ability to provide privacy-preserving compliance is becoming a primary competitive advantage for infrastructure providers.

Compare zk KYC infrastructure approaches

Selecting the right zero-knowledge infrastructure requires matching your technical stack with regulatory expectations. The market generally splits into three categories: standalone verification providers, integrated DeFi protocols, and enterprise-grade compliance suites. Each offers different tradeoffs in speed, privacy, and integration complexity.

Standalone ZK Providers

Standalone providers like Zyphe and Treza Labs focus on high-throughput verification with minimal data retention. They act as independent layers, issuing cryptographic proofs that applications can verify without storing raw identity documents. This approach suits platforms needing rapid integration and strict data minimization. Verification often occurs in sub-second intervals, reducing friction for end-users while maintaining regulator-grade audit trails.

Integrated DeFi Protocols

Integrated solutions embed zk-KYC directly into smart contracts or decentralized identity standards. This method prioritizes composability, allowing protocols to verify compliance status natively within their logic. While this reduces third-party dependency, it often limits flexibility for cross-platform reuse. These systems are best for protocols that prioritize on-chain verification and want to minimize off-chain data exposure.

Enterprise-Grade Solutions

Enterprise-grade platforms offer comprehensive compliance frameworks, often including KYB (Know Your Business) and advanced risk scoring. These systems are designed for institutional DeFi and traditional finance bridges, where regulatory acceptance is paramount. They typically involve higher integration complexity and cost but provide robust support for complex regulatory environments and multi-jurisdictional requirements.

| Feature | Standalone Providers | Integrated DeFi | Enterprise Suites |

|---|---|---|---|

| Verification Speed | Sub-second | Variable (on-chain) | Minutes to Hours |

| Data Retention | Minimal/None | None (on-chain) | High (regulated) |

| Integration Complexity | Low (API) | Medium (Smart Contracts) | High (Custom) |

| Regulatory Fit | General Compliance | On-Chain Native | Institutional/TradFi |

The right choice depends on your specific use case. For pure DeFi applications, integrated solutions offer the best privacy. For regulated financial products, enterprise suites provide the necessary auditability. Standalone providers offer a balanced middle ground for most Web3 platforms.

Strategic implementation for regulated finance

Adopting zero-knowledge KYC (ZK KYC) is less about installing new software and more about restructuring how an institution handles identity data. For regulated finance, the goal is to prove compliance without hoarding sensitive personal information. This shift requires a careful balance between cryptographic proof and existing legal frameworks.

Regulatory alignment and data minimization

Traditional KYC processes store vast amounts of unencrypted data, creating a high-value target for attackers. ZK KYC changes this by allowing institutions to verify attributes—such as age, residency, or accreditation status—without seeing the underlying documents. This aligns with the principle of data minimization, a core tenet of regulations like GDPR and emerging crypto-specific frameworks.

However, regulators are still catching up. Institutions must ensure their ZK circuits can produce proofs that satisfy specific legal thresholds. If a regulator demands proof of identity during an audit, the system must be able to generate a verifiable claim without exposing the raw data. This requires close collaboration with legal teams to define what constitutes "sufficient" verification in a zero-knowledge context.

Managing technical debt and user experience

The transition to ZK KYC introduces significant technical debt. Legacy systems are not built to handle zero-knowledge proofs, which require specialized cryptographic libraries and often off-chain computation. Integrating these components into existing customer onboarding flows can be complex and costly.

User experience is another critical factor. While ZK KYC offers superior privacy, the verification process can feel slower to users accustomed to instant document uploads. Institutions must optimize the proof generation process to keep friction low. A seamless experience is not just about speed; it is about trust. If users do not understand why their data is being processed differently, adoption will stall.

The infrastructure trade-off

The decision to implement ZK KYC is ultimately a trade-off between privacy and infrastructure complexity. For institutions dealing with high-volume, cross-border transactions, the benefits of reduced liability and enhanced privacy often outweigh the initial setup costs. However, for smaller firms, the technical overhead may be prohibitive.

As the market evolves, the cost of ZK proof generation is expected to decrease, making the technology more accessible. In the meantime, institutions should start by piloting ZK KYC in low-risk use cases, such as internal employee verification or specific DeFi partnerships, to build internal expertise before scaling to broader customer onboarding.

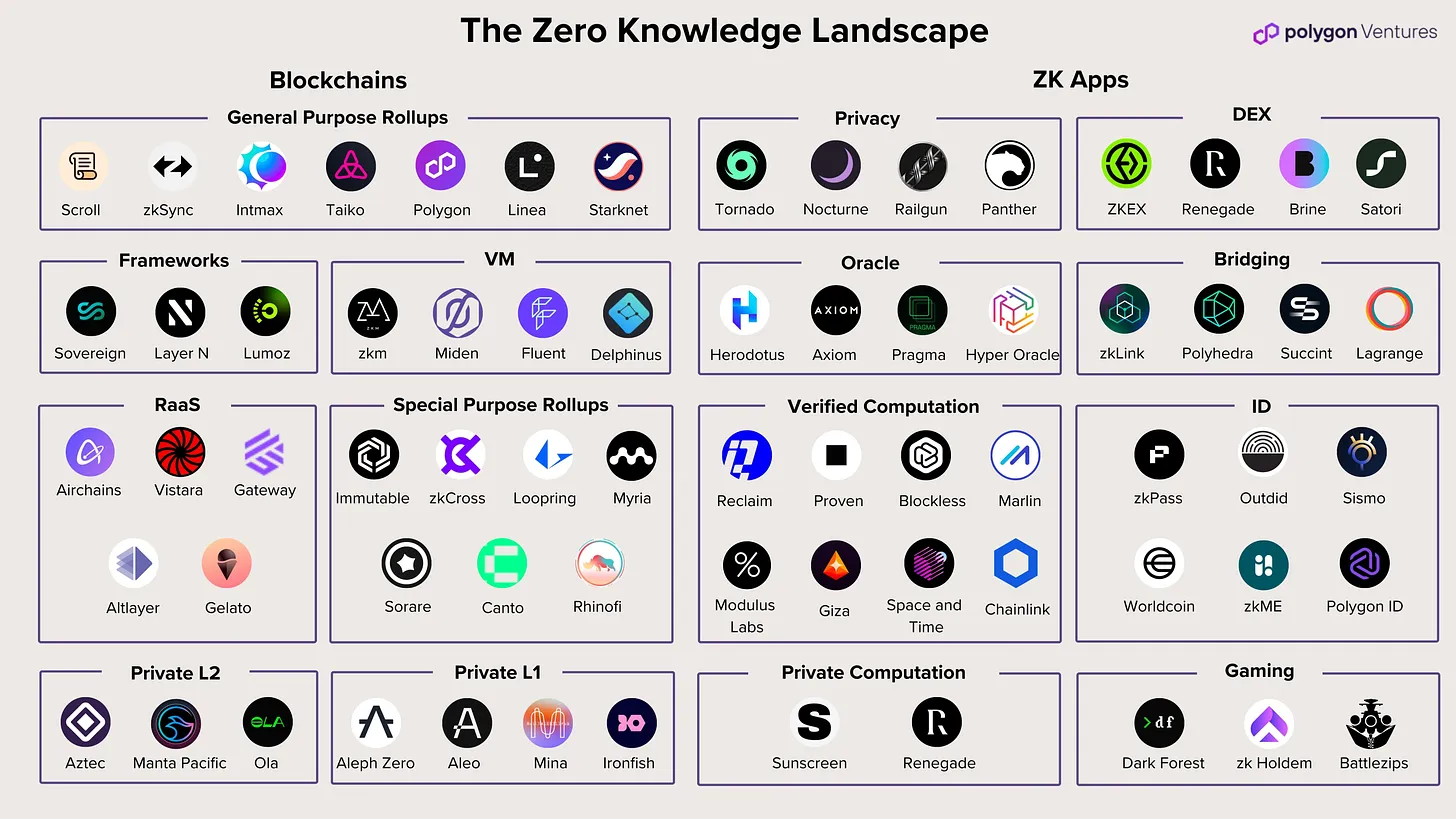

Key tools and vendors in the ZK KYC ecosystem

The ZK KYC landscape is shifting from theoretical prototypes to production-grade infrastructure. For developers and compliance officers, the choice of vendor dictates how easily cryptographic proofs integrate with existing compliance workflows. The market is currently defined by specialized providers that prioritize data minimization and sub-second verification speeds.

Trezalabs offers a foundational infrastructure layer for crypto and regulated finance. Their platform enables applications to verify that a user meets specific compliance requirements without exposing or storing personal data. This approach reduces liability by ensuring that sensitive identity documents never touch the application’s servers, relying instead on zero-knowledge proofs to validate eligibility.

For teams requiring a more integrated verification experience, Zyphe focuses on regulator-grade performance. Their production system handles identity checks with sub-second latency, a critical metric for user retention in high-volume environments. Zyphe’s architecture emphasizes no document retention, meaning the system generates the necessary cryptographic proof and discards the raw PII immediately, aligning technical execution with strict privacy regulations.

As an Amazon Associate, we may earn from qualifying purchases.

Frequently asked questions about ZK KYC

What is zk KYC?

Zero-knowledge KYC (zk KYC) is a privacy-first verification method that allows users to prove they meet specific identity criteria without revealing the underlying personal data. By leveraging zero-knowledge proofs, cryptographic techniques, and secure hardware enclaves (TEEs), systems can verify attributes like age or citizenship while keeping the actual documents private. This approach shifts the paradigm from data collection to data minimization, ensuring that sensitive information remains with the user rather than being stored by centralized third parties.

How big is the KYB market?

The broader Know Your Business (KYB) sector is expanding rapidly as regulatory scrutiny intensifies. According to Juniper Research, the global e-KYB market was valued at approximately USD 263.54 million in 2022 and is projected to reach USD 712.87 million by 2030. This growth, driven by a compound annual growth rate (CAGR) of roughly 13.28%, highlights the increasing demand for automated, compliant identity infrastructure across the financial sector.

Does zk KYC replace traditional KYC?

Not entirely, but it complements it. Traditional KYC often requires uploading sensitive documents like passports or utility bills to a central server. zk KYC replaces this with cryptographic proofs. Instead of handing over your ID, you generate a proof that confirms you are over 18 or reside in a specific jurisdiction. This reduces the attack surface for data breaches and aligns with emerging privacy regulations like GDPR, which emphasize data minimization and purpose limitation.

No comments yet. Be the first to share your thoughts!