Why ZK KYC Matters for Compliance

Traditional KYC processes operate on a binary choice: surrender your data or stay offline. This model creates a massive attack surface. When centralized databases hold sensitive identity documents, they become prime targets for breaches. A single leak can expose thousands of users to identity theft and financial fraud, eroding trust in the entire platform.

Zero-Knowledge Proof KYC changes this dynamic by introducing data minimization. Instead of uploading a passport or selfie, users generate a cryptographic proof that verifies they meet specific criteria—such as being over 18 or residing in a permitted jurisdiction—while keeping the raw data private. The verifier sees only the result: true or false.

For financial institutions, this is not just a technical upgrade; it is a risk management strategy. By adopting ZK KYC, platforms can satisfy Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements while significantly reducing their liability. As noted in industry analyses, this approach allows decentralized finance (DeFi) and traditional fintech to coexist, offering institutional-grade compliance without the privacy compromises of legacy systems.

How ZK KYC Infrastructure Works

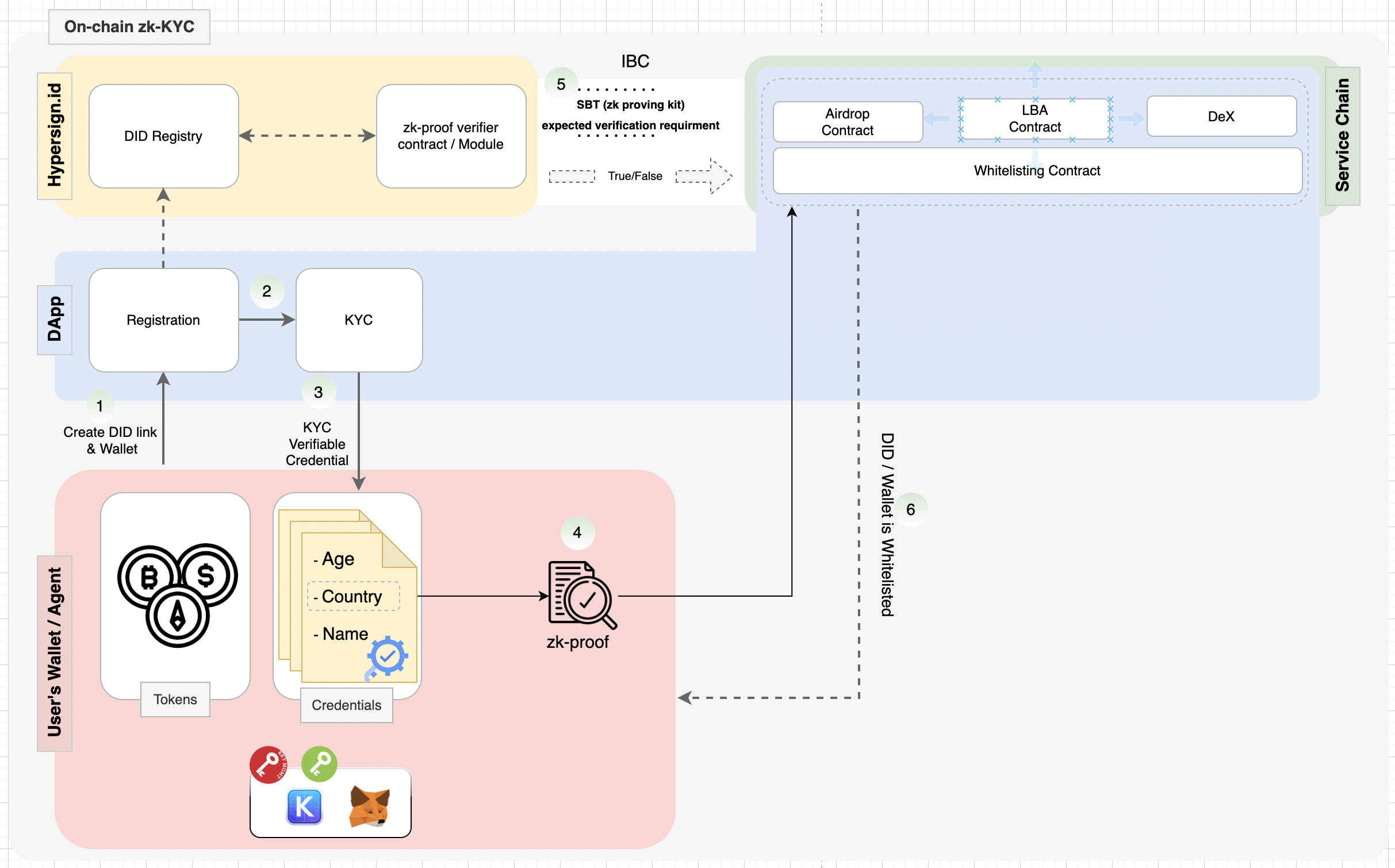

Zero-knowledge KYC (ZK KYC) infrastructure shifts the burden of trust from data storage to mathematical verification. Instead of keeping copies of passports or utility bills, the system generates a cryptographic proof that a user meets specific criteria—such as being over 18 or residing in a permitted jurisdiction—without exposing the personal data to the verifier.

The process follows a three-part flow: proof generation, verification, and on-chain validation. This architecture allows decentralized applications to comply with regulations while maintaining the privacy principles that define Web3.

1. Proof Generation

The journey begins when a user uploads encrypted credentials to the ZK KYC system. Providers like zkMe handle this initial step by accepting sensitive documents—such as government IDs or address proofs—and processing them through zero-knowledge circuits.

These circuits act as a filter. They take the raw data as input and run it against predefined logical rules. If the data satisfies the conditions, the circuit outputs a "proof." Crucially, this proof is a compact cryptographic string. It contains no personal information, only the mathematical confirmation that the user passed the check. As noted by providers like Zyphe, this step can achieve regulator-grade verification with sub-second performance, ensuring the user experience remains smooth.

2. Verification

Once the proof is generated, it must be validated. In many ZK KYC models, a decentralized network of verifiers or a trusted oracle validates the proof against the public parameters of the zero-knowledge protocol. This step ensures that the proof is genuine and hasn't been tampered with.

The verifier does not see the user's ID number or name. It only checks the mathematical integrity of the proof. If the proof is valid, the system issues a "ZK-SNARK" or similar tokenized credential. This credential serves as a portable, privacy-preserving badge of compliance that the user can hold in their wallet.

3. On-Chain Validation

The final step occurs when the user interacts with a decentralized application (dApp). The dApp requires proof of compliance before allowing access. The user presents their ZK credential, and the dApp’s smart contract verifies it on-chain.

Because the verification logic is embedded in the smart contract, the process is trustless and automatic. The dApp receives a simple boolean result: true or false. It never sees the underlying identity data. This architecture enables seamless integration of compliance into DeFi, NFT marketplaces, and other on-chain services without creating central points of failure for personal data.

This three-step flow demonstrates why ZK KYC is gaining traction among institutions. It decouples identity from data retention, reducing liability for both the service provider and the user. By keeping personal data off-chain and only sharing proofs on-chain, ZK KYC infrastructure aligns technical architecture with regulatory requirements.

Key ZK KYC Providers and Solutions

ZK KYC Systems works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

The Compliance Paradox: Privacy vs. Regulation

Zero-knowledge KYC systems face a fundamental tension: regulators demand visibility, while users demand opacity. Traditional compliance relies on sharing sensitive data to prove eligibility. ZK-KYC flips this model by proving compliance without exposing the raw data. However, this shift creates new legal hurdles, particularly around Anti-Money Laundering (AML) frameworks and the concept of "lawable intercept."

Navigating AML and Data Minimization

Financial institutions must balance regulatory obligations with privacy principles. The General Data Protection Regulation (GDPR) enshrines data minimization, meaning organizations should only collect what is strictly necessary. Traditional KYC processes often violate this by hoarding vast amounts of personal information.

ZK-KYC aligns with these principles by allowing users to prove they are not on a sanctions list or meet age requirements without disclosing their name or address. As noted by Studio AM, this approach offers a new paradigm for institutional DeFi, enabling compliance without the privacy risks of centralized data storage. This reduces the attack surface for data breaches while satisfying regulatory audits.

eIDAS 2 and Verifiable Credentials

The European Union’s eIDAS 2 regulation introduces the European Digital Identity Wallet (EUDI), which relies heavily on verifiable credentials. This framework is designed to work seamlessly with privacy-preserving technologies like zero-knowledge proofs.

Under eIDAS 2, users can present attested claims—such as residency or accreditation—without exposing the original document. For ZK KYC providers, this means building systems that can verify these specific credential formats. The goal is to create a system where the verifier trusts the issuer’s signature but never sees the raw data. This creates a "privacy-by-default" environment that complies with EU law while protecting user identity.

The Challenge of Lawful Intercept

The most contentious issue in ZK KYC is "lawful intercept." Regulators expect the ability to trace illicit transactions and identify bad actors. In a fully anonymous ZK system, this is technically difficult.

To address this, some architectures propose a "key recovery" or "escrow" mechanism, where a trusted third party holds the decryption key for law enforcement. However, this reintroduces the centralization risks ZK KYC aims to eliminate. Most privacy-first providers argue for a different approach: allowing users to selectively disclose identity only when a legal threshold is met, rather than maintaining a master key that could be abused. This requires careful legal framing to ensure the system remains compliant without becoming a surveillance tool.

Market Trends and Future Outlook

The market for ZK KYC systems is shifting from experimental pilots to institutional necessity. As regulatory pressure on DeFi protocols intensifies, the ability to verify identity without exposing sensitive personal data has become a primary adoption driver. This technology bridges the gap between open finance and traditional compliance requirements, allowing institutions to participate in decentralized markets while adhering to data protection standards.

Adoption is accelerating among providers building privacy-first infrastructure. Early implementations demonstrate that zero-knowledge proofs can satisfy Know Your Customer (KYC) and Anti-Money Laundering (AML) obligations without creating centralized data silos. This shift is critical for regulated finance, which seeks to integrate blockchain assets without compromising user privacy or creating single points of failure.

Looking ahead, the integration of ZK KYC into mainstream financial services will likely define the next phase of blockchain maturity. Protocols that prioritize this architecture will be better positioned to onboard institutional capital. The trend suggests a future where compliance is embedded into the cryptographic layer of financial applications rather than treated as an afterthought.

No comments yet. Be the first to share your thoughts!