Why traditional KYC breaks down

The current identity verification model is built on a fundamental contradiction: it requires collecting sensitive personal data to prove you are who you say you are, while simultaneously creating a massive, centralized target for attackers. Traditional Know Your Customer (KYC) workflows demand the storage of passports, bank statements, and proof of residence. These documents are not just records; they are high-value assets that attract sophisticated cybercriminals.

When a centralized database holds millions of identities, the liability is enormous. A single breach doesn't just expose names; it compromises the financial and legal standing of every user in the system. As noted by identity infrastructure providers, this concentration of PII creates a "honeypot" effect, making legacy systems inherently fragile regardless of their security upgrades.

Regulatory Liability: Storing PII in centralized databases is no longer just a security risk; it is a regulatory liability. Compliance frameworks like GDPR and CCPA impose heavy fines for data mishandling, meaning the cost of a breach extends far beyond remediation to existential legal threats.

This risk profile is why the industry is shifting toward zero-knowledge architectures. Instead of hoarding data, ZK-KYC allows institutions to verify cryptographic claims about a user without ever collecting the underlying PII. You verify the claim, not the document. This shift moves the burden of privacy from the user to the protocol, eliminating the central point of failure that has plagued traditional compliance for decades.

How zk KYC actually works

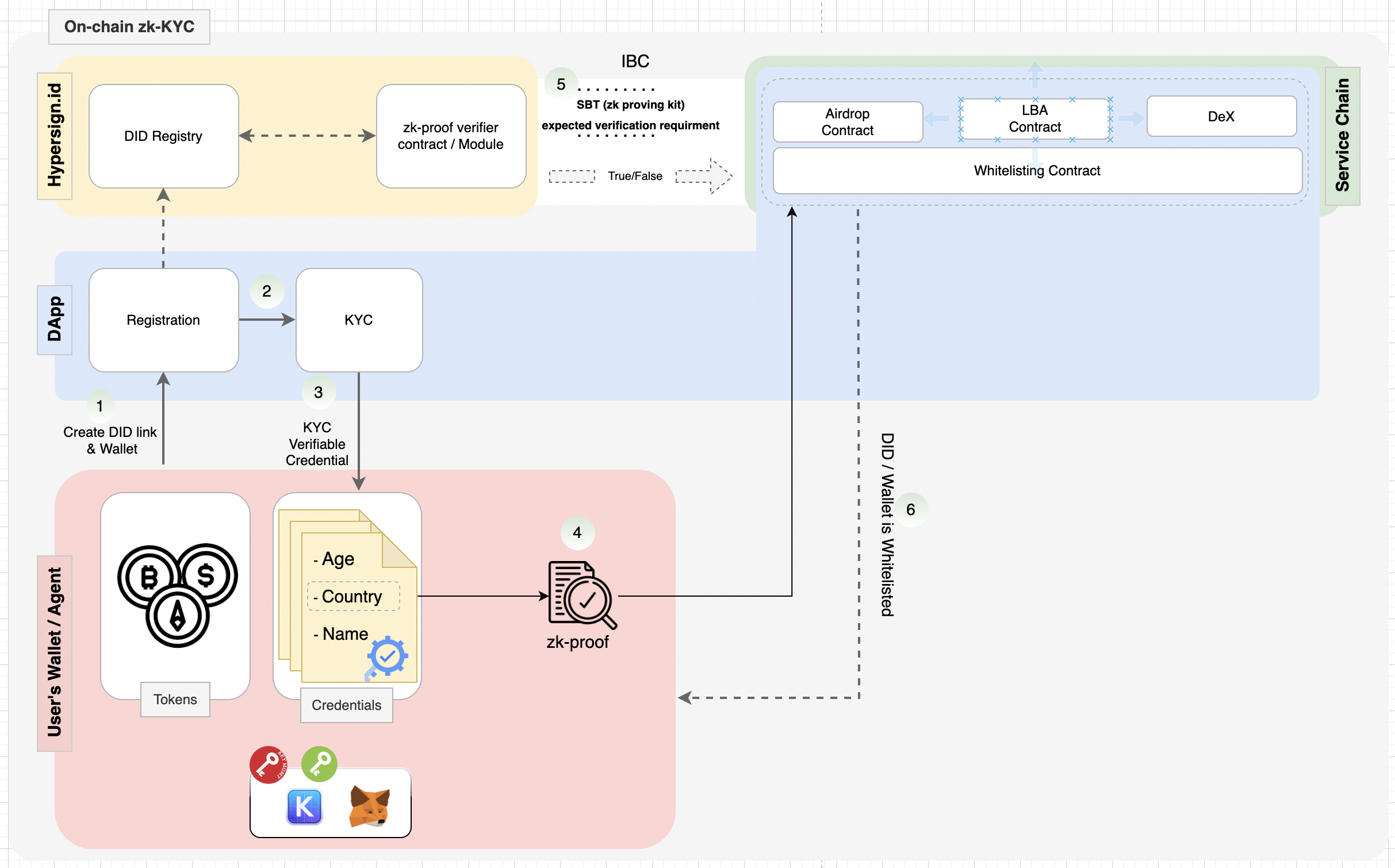

The architecture of zero-knowledge KYC (ZK-KYC) transforms identity verification from a data collection exercise into a cryptographic proof. Instead of handing over raw personal documents to every service provider, users interact with a system that validates their status without revealing the underlying data. This flow ensures regulatory compliance while keeping sensitive information off-chain and out of public view.

The process relies on three distinct phases: issuance, proof generation, and on-chain verification. Each step is designed to minimize the attack surface for data breaches while maintaining the auditability required by financial regulators.

The process begins with a trusted issuer, such as a government agency or a regulated identity provider. After completing a traditional Know Your Customer (KYC) check, the issuer signs a verifiable credential and sends it to the user’s digital wallet. This credential contains the necessary claims—like age or accreditation status—encrypted and secured by the issuer’s private key.

When the user needs to access a service, their wallet software generates a zero-knowledge proof using the stored credential. This cryptographic computation demonstrates that the user meets specific criteria (e.g., "is over 18" or "is a qualified investor") without exposing the actual birthdate or government ID number. The proof is mathematically sound but reveals nothing beyond the boolean result of the check.

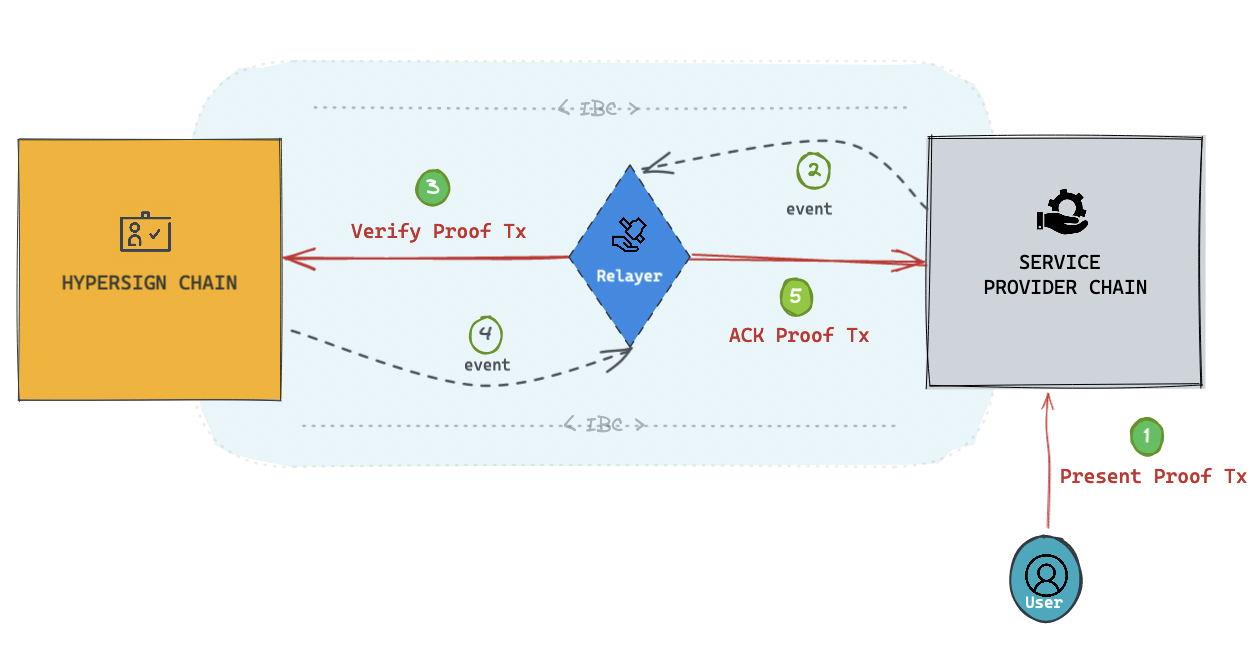

The generated proof is submitted to a smart contract or a verification oracle. The contract checks the proof against the issuer’s public key and the predefined rules. If the proof is valid, the contract grants access to the permissioned pool or service. This happens in seconds, with no personal data ever touching the public ledger or the service provider’s database.

This flow creates a strict separation between identity and activity. As noted by Chainlink, this method allows institutions to verify that liquidity providers are vetted entities without exposing their identities to other traders in the pool. For high-stakes financial environments, this reduces the risk of regulatory non-compliance while simultaneously protecting user privacy.

The three layers of ZK KYC infrastructure

Building a privacy-first compliance system requires stitching together three distinct technical layers. Each layer handles a specific part of the verification chain, from issuing credentials to proving them on-chain. Getting this architecture right is not just about code; it is about managing the high stakes of financial regulation while preserving user anonymity.

Identity Providers (Issuers)

The process begins with an Identity Provider, often a regulated entity like a bank or a licensed KYC vendor. This issuer verifies the user’s real-world identity using traditional methods—checking passports, biometrics, and sanctions lists. Once verified, the issuer does not store the raw data for the next step. Instead, it issues a cryptographically signed credential to the user’s wallet. This credential acts as a digital passport, proving the user has passed due diligence without revealing their name or address to the rest of the system. As noted by Treza Labs, this shift means the infrastructure verifies claims rather than collecting sensitive PII [1].

ZK Circuits and Provers

The second layer is the most complex: the Zero-Knowledge circuit and its prover. Here, the user’s wallet takes the signed credential and generates a zero-knowledge proof. This proof demonstrates that the credential is valid and meets specific criteria—such as being over 18 or not being on a sanctions list—without exposing the underlying data. The prover essentially says, “I have a valid credential,” without showing the credential itself. This step is critical for privacy, as it ensures that no personal information leaks during the verification process. The circuit logic must be rigorously audited, as any flaw could allow fraudulent proofs to bypass compliance checks.

On-Chain Verifiers

The final layer is the on-chain verifier, typically a smart contract deployed on the blockchain. This contract holds the public verification key for the ZK circuit. When a user submits their proof to interact with a DeFi protocol or exchange, the verifier checks the proof against the key. If the proof is mathematically valid, the contract grants access. This allows protocols to enforce compliance rules automatically and transparently. Because the verifier only sees the proof, not the user’s identity, the system maintains privacy while satisfying regulatory requirements. This architecture enables permissioned pools where all participants are vetted, but their identities remain hidden from each other [2].

| Layer | Traditional KYC | ZK KYC Infrastructure |

|---|---|---|

| Identity Provider | Collects and stores raw PII (passport, selfie) in central databases. | |

| Identity Provider | Issues signed cryptographic credentials to user wallets after verification. | |

| Verification Logic | Manual or API-based checks against internal or third-party databases. | |

| Verification Logic | User generates ZK proofs using private circuits; no data is exposed. | |

| On-Chain Result | Centralized ledger updates user status; high risk of data breaches. | |

| On-Chain Result | Smart contract verifies proof; access granted without revealing identity. |

Strategic use cases in regulated DeFi

The transition from experimental protocols to institutional-grade infrastructure requires more than just privacy; it demands compliance that satisfies regulators without alienating users. ZK-KYC systems are currently enabling three distinct use cases that bridge this gap: permissioned liquidity pools, streamlined institutional onboarding, and cross-chain regulatory alignment.

Permissioned Liquidity Pools

Permissioned pools allow protocols to restrict access to specific groups of users—such as accredited investors or residents of approved jurisdictions—without revealing their identities to the broader market. An institution can issue a verifiable credential to a user’s wallet, which the user then uses to generate a zero-knowledge proof of eligibility. This ensures all liquidity providers are vetted entities without exposing their identities to other traders or the public ledger [[src-serp-2]]. This mechanism is critical for DeFi protocols seeking to operate within jurisdictions that require strict KYC/AML adherence while maintaining the benefits of decentralized trading.

Institutional Onboarding

For traditional finance players, the friction of onboarding into DeFi has historically been a major barrier. ZK-KYC simplifies this by allowing institutions to prove their regulatory status (e.g., being a registered entity) without disclosing sensitive internal data or transaction histories to the protocol operators. This reduces the operational overhead for both the institution and the DeFi platform, fostering a more secure environment where only compliant actors can participate in high-value transactions. It effectively creates a "whitelisted" layer of trust that sits atop the transparent blockchain.

Cross-Chain Compliance

As assets move between different blockchain networks, maintaining a consistent compliance record becomes challenging. ZK-KYC enables the portability of verified identity states across chains. A user verified on one chain can generate a proof that is valid on another, eliminating the need for redundant verification processes. This interoperability is essential for a unified DeFi ecosystem, ensuring that compliance is not siloed within a single network but is a portable attribute that travels with the user’s digital identity.

Compliance and regulatory alignment

Zero-knowledge KYC systems are designed to satisfy the same AML and KYC mandates that govern traditional finance, but they do so without forcing users to surrender their personal data. Instead of storing passports or selfies in a central database, these systems rely on cryptographic proofs to verify that a user meets specific regulatory criteria—such as being over 18, not on a sanctions list, or holding a valid license.

This approach aligns directly with emerging frameworks like eIDAS 2, which emphasizes secure digital identity and privacy-by-design principles. By shifting from data collection to data verification, institutions can demonstrate compliance to regulators while ensuring that sensitive information never leaves the user’s control. This reduces the attack surface for data breaches and minimizes liability.

The primary challenge lies in mapping these cryptographic proofs to specific legal requirements. Regulators are increasingly accepting zero-knowledge proofs as valid evidence of identity, provided the underlying verification process is auditable and robust. As AMLA trends shift toward more sophisticated monitoring, ZK systems offer a way to maintain high-stakes compliance without compromising the privacy that users expect in digital interactions.

No comments yet. Be the first to share your thoughts!