Why traditional KYC fails in Web3

The core problem with traditional KYC isn't just bureaucracy; it's architecture. Centralized systems require identity providers to store vast amounts of personally identifiable information (PII)—passports, bank statements, and proof of residence—in centralized databases. This creates a single point of failure that is unacceptable for high-stakes Web3 applications where data privacy is paramount.

When you hand your identity documents to a centralized verifier, you are no longer in control of that data. As noted in industry documentation, these storage requirements create high-value targets for malicious actors. A single breach can expose millions of users' sensitive information, leading to irreversible identity theft and regulatory penalties. In the Web3 context, where anonymity is often a feature rather than a bug, this centralized exposure is a fundamental contradiction.

For Web3 applications, the risk extends beyond simple data leaks. Centralized KYC introduces regulatory friction and operational bottlenecks that slow down user onboarding. More critically, it undermines the trustless nature of decentralized finance. Users are asked to surrender their privacy for access, creating a power imbalance that centralized entities exploit. This model is unsustainable for a sector built on user sovereignty and cryptographic security.

The solution requires a shift from "trust us" to "verify mathematically." By using zero-knowledge proofs, systems can verify compliance without ever seeing the underlying data. This approach eliminates the central repository of PII, removing the incentive for hackers and reducing the regulatory burden on service providers. It aligns security with privacy, ensuring that compliance does not come at the cost of user autonomy.

How ZK proofs verify identity without data

Zero-knowledge proofs (ZKPs) allow a user to prove a specific claim about their identity without revealing the underlying personal information. In a traditional KYC flow, you submit a passport or driver’s license to a verifier, who then stores that sensitive data. With ZK-KYC, the verifier receives a cryptographic proof that confirms you meet certain criteria—such as being over 18 or not on a sanctions list—without ever seeing the actual document.

Think of it like a nightclub bouncer. You don’t hand over your ID and let them photocopy it. Instead, you prove you’re of age in a way that confirms the fact without exposing your name, address, or birthdate. The verifier accepts the proof as valid evidence of compliance, and the underlying data remains private.

This mechanism relies on complex mathematics to generate a proof that is both compact and verifiable. The user’s identity data stays on their device or in a secure, decentralized identity system. Only the proof is shared with the service provider, such as a DeFi platform or financial institution. This approach significantly reduces the risk of data breaches and misuse of personal information.

The infrastructure supporting ZK-KYC typically involves an identity issuer (like a government or accredited entity) that attests to user attributes. The user then generates a zero-knowledge proof based on these attestations. A smart contract or off-chain verifier checks the proof’s validity against public parameters. If the proof is valid, the user is granted access or status without the verifier learning anything beyond the truth of the statement.

Infrastructure components for ZK KYC

Building a zero-knowledge KYC system requires stitching together three distinct layers: identity providers, circuit designers, and oracle networks. Each component handles a specific part of the privacy puzzle, ensuring that personal data remains off-chain while the proof of compliance lives on-chain.

Identity Providers

Identity providers are the trusted sources that issue verifiable credentials. In a ZK KYC context, these are typically government agencies or regulated financial institutions that hold the raw personal data. The provider signs a credential—such as a passport hash or age verification token—without revealing the underlying details to the blockchain. This creates a secure anchor for the entire system, ensuring that the zero-knowledge proof is built on verified, real-world data rather than anonymous claims.

Circuit Designers

Circuit designers translate legal requirements into mathematical constraints. These are the "zk-circuits" that define exactly what data is needed to satisfy a KYC check. For example, a circuit might verify that a user is over 18 and not on a sanctions list, without revealing their birthdate or name. Tools like Circom or SnarkJS allow developers to write these logic gates. The output is a cryptographic proof that attests to the truth of the statement, keeping the input data private. This layer is where regulatory compliance meets computational efficiency.

Oracle Networks

Oracle networks bridge the gap between off-chain data and on-chain verification. Services like Chainlink DECO enable users to prove statements about their private data without exposing the data itself. The oracle fetches the necessary information from the identity provider, helps generate the zero-knowledge proof, and submits it to the smart contract. This ensures that the verification process is secure and decentralized, preventing any single point of failure or censorship. The oracle acts as a neutral intermediary, maintaining the integrity of the privacy-preserving workflow.

Infrastructure Layer Comparison

Understanding how these components interact helps clarify the trade-offs in ZK KYC architecture. The table below contrasts the primary roles and verification methods of each layer.

| Layer | Primary Role | Verification Method |

|---|---|---|

| Identity Providers | Issue verifiable credentials | Digital signatures from trusted authorities |

| Circuit Designers | Define privacy constraints | Mathematical proof generation (zk-SNARKs/STARKs) |

| Oracle Networks | Fetch and relay data | Decentralized node consensus (e.g., Chainlink DECO) |

The ZK KYC Market Landscape

The infrastructure for zero-knowledge KYC has moved from theoretical research to production-ready tools. Rather than relying on a single monolithic provider, the market now offers specialized components that verify specific claims—age, residency, or legal status—without touching the underlying personal data. This modular approach reduces the liability of holding sensitive documents while maintaining regulatory compliance.

Core Infrastructure Providers

Leading platforms like Treza Labs and Zyphe have built the foundational layers for this verification model. Treza Labs focuses on the crypto and regulated finance sectors, enabling protocols to verify cryptographic claims about a user without collecting or storing the underlying PII. This architecture allows for "verify once, use many" workflows, where a user's identity status is attested cryptographically rather than through repeated document uploads.

Zyphe operates similarly but emphasizes speed and regulatory-grade verification. Their system delivers sub-second performance, a critical requirement for user-facing applications, while ensuring no document retention. By eliminating the storage of passports or bank statements, these providers remove the primary target for data breaches. The result is a compliance framework that satisfies regulators without creating a honeypot for attackers.

Specialized Verification Tools

Beyond the core infrastructure, specialized tools like zkPass and Hypersign Protocol address specific integration challenges. zkPass focuses on automating the verification of off-chain data sources, such as bank statements or government portals, by extracting and proving the validity of specific fields without exposing the full document. This is particularly useful for high-stakes lending or investment platforms that require proof of income or assets.

Hypersign Protocol offers a decentralized identity layer that integrates with existing blockchain networks. Their approach allows users to hold their own verified credentials in a digital wallet, presenting only the necessary proof to a verifier. This shifts the control of identity data back to the user, aligning with the privacy-first ethos of the Web3 space while still meeting Know Your Customer (KYC) requirements.

Choosing the Right Tool

Selecting a ZK KYC solution depends on your specific compliance needs and technical stack. If you are building a regulated financial product, prioritize providers with established regulatory partnerships and audit trails. For decentralized applications, look for tools that support decentralized identifiers (DIDs) and verifiable credentials. The goal is to minimize data exposure while maximizing verification confidence.

As an Amazon Associate, we may earn from qualifying purchases.

Integrating ZK KYC into Existing Workflows

Compliance teams face a high-stakes challenge: adopting zero-knowledge proof systems without breaking established AML/KYC protocols. The goal is to layer privacy-preserving verification onto legacy infrastructure, ensuring that sensitive identity data remains siloed while regulatory signals flow freely.

Start by auditing your current data flow. Identify which fields trigger regulatory flags and which are purely operational. ZK KYC works best when you separate the "verifiable claim" (e.g., age, residency) from the raw PII. This separation allows you to generate a proof that satisfies compliance officers without exposing the underlying database to unnecessary risk.

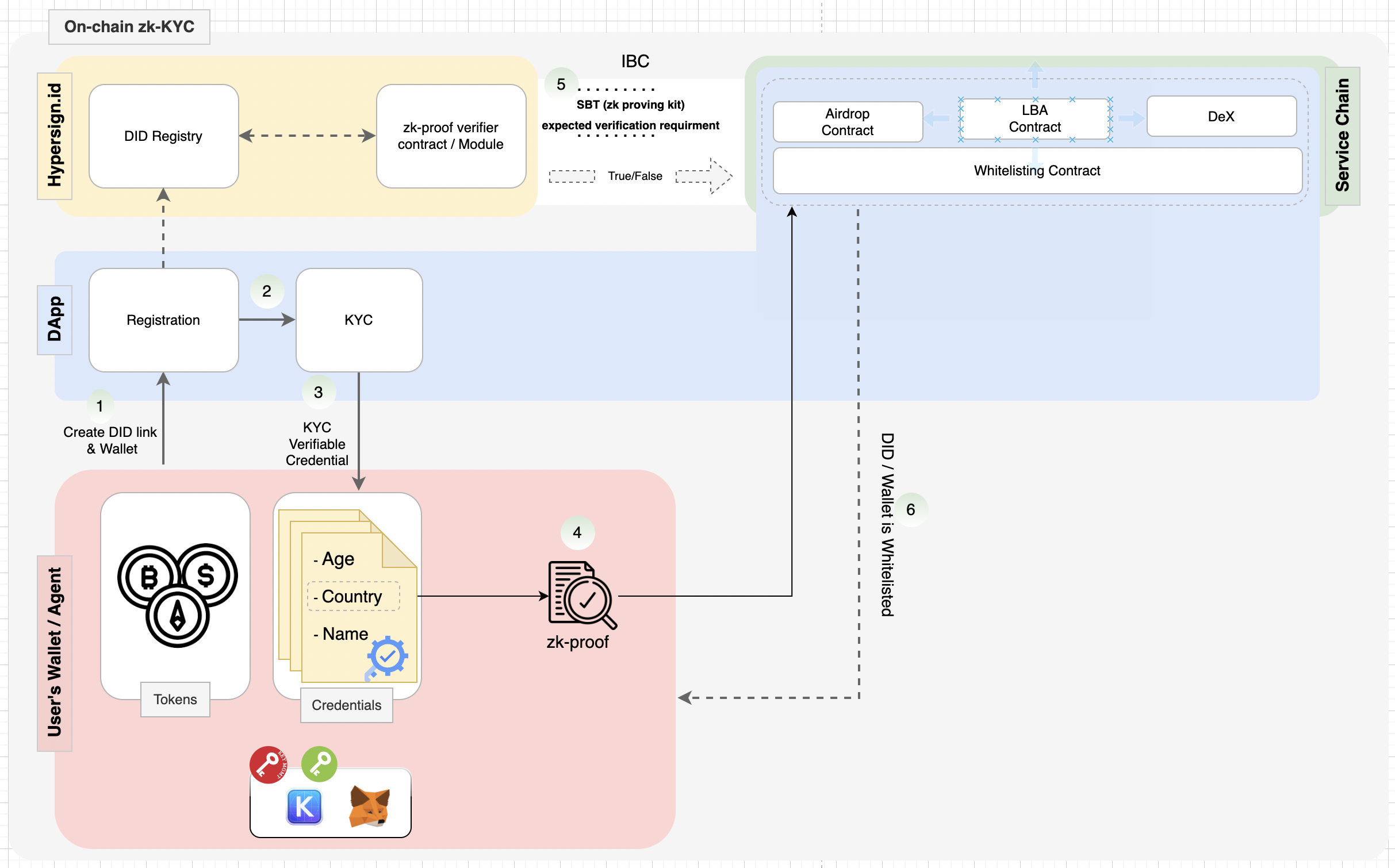

Next, design the architecture to support a "Service Chain." As noted in industry analyses, a dedicated identity system can serve a separate chain where DeFi applications operate. This isolates the heavy cryptographic computation from the main transaction layer, preventing network congestion while maintaining a clear audit trail for regulators.

Finally, implement a "no master key" policy. Ensure that no single entity holds the ability to decrypt all user identities. This design choice is critical for mitigating the risk of a central point of failure. By distributing trust and using zero-knowledge proofs, you create a system that is both compliant and resilient against data breaches.

No comments yet. Be the first to share your thoughts!